The IRS estimates the tax gap from the individual income tax (the amount of true income tax liability that goes unpaid) was $245 billion annually from 2011-2013. The gross tax gap has three components: non-filing, underpayment, and underreporting, of which underreporting makes up 80 percent. Income underreporting on income tax returns has implications for income tax collection at the state level.

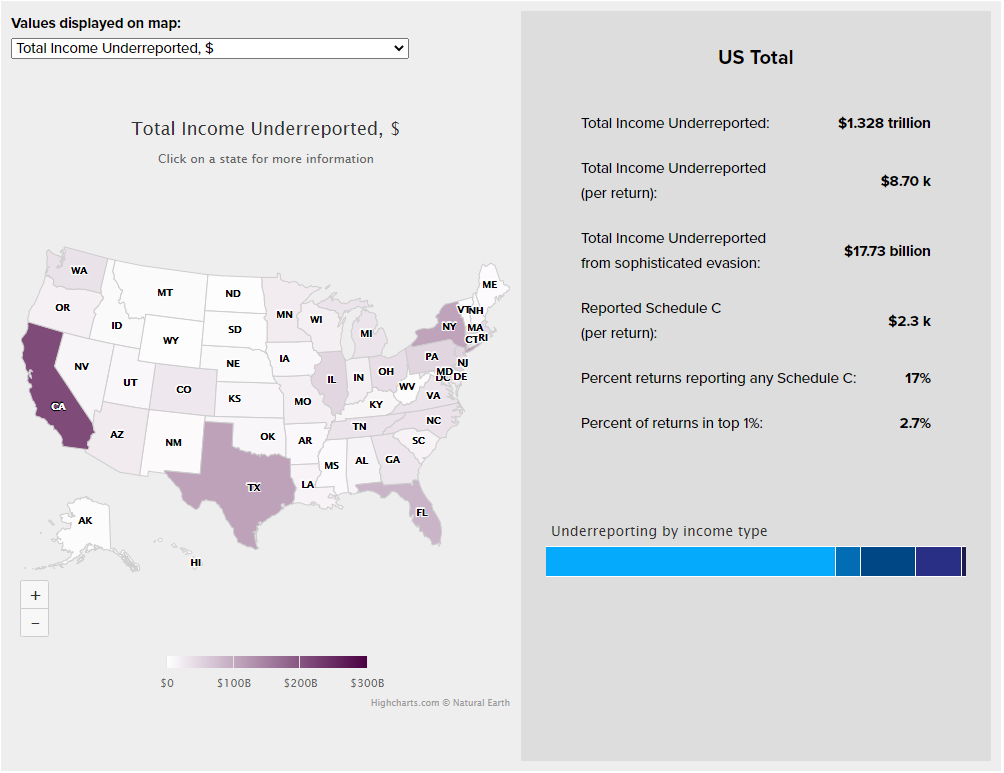

Combining SOI aggregate data for tax year 2018 with new estimates of income underreporting, Figure 1 presents a map of state-level data with PWBM’s estimates of income underreporting and related trends. Use the drop-down menu to choose between which estimate or statistic the map displays. All numbers are for tax year 2018.

Please view online for interactivity.

(per return):

from sophisticated evasion:

(per return):

We estimate $1.33 trillion of income goes underreported on federal income tax returns. Nationally, we estimate that Schedule C business income constitutes 69 percent of underreported income in 2018. Underreporting of Partnership and S-Corp income is 13 percent of total underreporting, and 11 percent is underreporting of financial income (capital gains, dividends, and interest).1 States with high levels of reported Schedule C income are the same states with high per-return income underreporting (a 1 percentage point increase in average schedule C income per return predicts a 0.96 percentage point increase in total per-return underreporting). However, states with high rates of schedule C filers are not the same states with high reported (and therefore underreported) amounts of Schedule C income (correlation between the two is 0.25).

Further, states with higher percentages of returns in the highest AGI groups are also correlated with high per-filer underreporting from sophisticated evasion (with a correlation of 0.76). This result accords with Guyton et al. (2021)’s findings of sophisticated evasion practices among the top 1 percent.

SOI historical table 2 has aggregate amounts of reported income of major income types, presented by state and by AGI class. For income types that are net values (capital gains income, partnership and S-corp income, and Schedule C business income) we adjust using national aggregates from SOI Table 1.4 to produce estimates of positive income.2

To these income amounts, we apply estimates of income underreporting rates from Guyton et al. (2021). These multipliers come from IRS estimates of income underreporting from the National Research Program with detection-controlled estimation (DCE) correction. Income type-specific estimates of underreporting rates are presented separately for the top 1 percent by total true income and the full population. We apply these rates to income reported in the SOI bulletin based on their Adjusted Gross Income (AGI) class. In 2018, the top 1 percent of the overall income distribution were families with AGI above $488,000; we apply underreporting factors to the SOI aggregates AGI groups with $500,000 AGI and above (top 1 percent) and all lower AGI groups are presumably the bottom 99 percent.3

We present underreporting estimates for the following income types: Wages and salaries, capital gains, income from partnerships and S-corps, dividend income, Schedule C business income, interest income, and other income (which is comprised of Pensions and IRA distributions, Social Security, unemployment income, and income from state and local tax refunds).4

The above methodology produces income-specific estimates of tax evasion in accordance with DCE-corrected IRS detection. To account for Guyton et al. (2021) benchmark estimates of sophisticated evasion, we apply the ratio of their benchmark estimates to the DCE-corrected evasion estimates separately between the top 1 percent and the 99 percent to compute sophisticated evasion totals. We distribute the sophisticated evasion totals proportionally between capital gains income, interest income, dividend income, and pass-through business income.

This analysis was conducted by Victoria Osorio. Prepared for the website by Mariko Paulson.

-

These estimates of underreporting by income type are proportional, on average, to the amount of each income type reported in the SOI aggregates in that state. ↩

-

In SOI Table 1.4, net gains and net losses are aggregates of returns with a net gain and net loss, respectively. Even the sum of net gains are net values offset by losses within each return. As a result, these estimates of positive income are effectively lower-bound estimates, as we cannot accurately estimate the amount of positive income from the aggregates of net values. ↩

-

The underreporting rates calculated by [GLRRZ21] are reported separately between the top 1 percent and full population as ranked by true income. The SOI aggregate data only observes reported income, and so we apply the income-specific underreporting rates according to the tax return’s place in the reported income distribution. ↩

-

While Guyton et al. (2021) estimates also present underreporting rates for some additional minor income types such as rental income, the aggregates for these income types are not provided in the SOI data and therefore we cannot include them in our analysis. Further, we are unable to estimate overreporting of deductions and credits, which would further increase estimates of income underreporting. ↩

US Total 1327955476.79381 8.70 17733000 0.69 0.06 0.13 0.11 0.01 2.3 0.17 0.027

AK 2990569 8.57 27595.23 0.76 0.05 0.12 0.07 0.007 2.4 0.16 0.007

AL 12503364 6.06 140991.9 0.69 0.07 0.15 0.08 0.01 1.6 0.17 0.006

AR 7820082 6.32 81407.79 0.67 0.06 0.13 0.13 0.008 1.6 0.17 0.006

AZ 23416401 7.57 259843.6 0.69 0.06 0.13 0.11 0.01 1.9 0.16 0.008

CA 2.12E+08 11.69 2993563 0.72 0.05 0.12 0.1 0.009 3.3 0.19 0.016

CO 28341541 10.25 307236.9 0.68 0.05 0.15 0.11 0.008 2.7 0.18 0.012

CT 22759353 12.87 371102.4 0.72 0.05 0.09 0.12 0.012 3.7 0.16 0.019

DC 4955580 14.16 110950.1 0.71 0.05 0.13 0.1 0.013 4.1 0.19 0.022

DE 2918187 6.21 27408.62 0.66 0.07 0.15 0.1 0.013 1.6 0.13 0.007

FL 87620758 8.57 1478852 0.6 0.05 0.19 0.15 0.013 1.9 0.22 0.011

GA 29936436 6.53 411566.1 0.63 0.07 0.18 0.11 0.01 1.5 0.23 0.009

HI 6093031 8.77 55996.13 0.77 0.05 0.09 0.08 0.01 2.6 0.16 0.006

IA 9350302 6.41 80508.42 0.67 0.07 0.15 0.1 0.009 1.6 0.14 0.006

ID 6179570 7.89 61581.65 0.65 0.05 0.19 0.1 0.008 1.9 0.17 0.007

IL 48310502 7.9 714998.6 0.65 0.07 0.14 0.13 0.011 2 0.16 0.011

IN 18927363 6.01 192376.1 0.68 0.07 0.16 0.08 0.009 1.6 0.13 0.006

KS 10255857 7.68 114531.5 0.68 0.06 0.15 0.1 0.008 2 0.15 0.008

KY 12094406 6.29 113066.7 0.71 0.06 0.12 0.1 0.008 1.7 0.15 0.005

LA 14013871 7.14 178537.5 0.7 0.06 0.16 0.07 0.009 1.8 0.2 0.007

MA 42721495 12.25 686141.3 0.7 0.05 0.12 0.12 0.009 3.4 0.16 0.017

MD 24848879 8.27 335788.6 0.7 0.07 0.14 0.09 0.012 2.2 0.2 0.011

ME 5554341 8.33 37503.8 0.77 0.05 0.1 0.08 0.007 2.4 0.17 0.006

MI 32301363 6.75 375810.5 0.69 0.06 0.14 0.1 0.01 1.8 0.15 0.007

MN 21892373 7.83 239131.5 0.67 0.07 0.16 0.1 0.009 2 0.15 0.01

MO 19314948 6.87 214226.1 0.69 0.06 0.14 0.1 0.01 1.8 0.15 0.007

MS 6765406 5.51 66353 0.73 0.06 0.13 0.07 0.009 1.5 0.19 0.004

MT 4361657 8.53 46509.12 0.68 0.04 0.17 0.11 0.008 2.2 0.17 0.007

NC 33589710 7.24 342467.5 0.7 0.06 0.14 0.09 0.009 1.9 0.18 0.008

ND 2732818 7.51 28442.2 0.65 0.06 0.18 0.1 0.007 1.9 0.15 0.009

NE 5882278 6.47 59311.96 0.62 0.07 0.18 0.12 0.009 1.5 0.15 0.007

NH 8020313 11.26 91136.07 0.79 0.05 0.06 0.09 0.007 3.5 0.15 0.01

NJ 49169118 11.02 712441.8 0.72 0.06 0.12 0.08 0.01 3.2 0.16 0.016

NM 5613929 6.04 51036.78 0.73 0.06 0.11 0.09 0.01 1.7 0.15 0.005

NV 11361987 7.84 181158 0.62 0.05 0.16 0.16 0.011 1.8 0.17 0.009

NY 1.08E+08 11.1 1986214 0.68 0.05 0.13 0.12 0.012 3 0.17 0.015

OH 38470307 6.84 391477.8 0.72 0.06 0.12 0.09 0.009 1.9 0.14 0.007

OK 11092706 6.76 109673.6 0.7 0.06 0.14 0.09 0.009 1.7 0.18 0.007

OR 17361591 8.83 155588.9 0.71 0.05 0.14 0.1 0.009 2.4 0.15 0.008

PA 49184753 7.86 562376.5 0.72 0.06 0.11 0.1 0.01 2.2 0.13 0.009

RI 4405489 8.13 43183.12 0.74 0.06 0.11 0.09 0.008 2.3 0.15 0.008

SC 15302737 6.72 166094 0.69 0.06 0.15 0.09 0.011 1.7 0.17 0.007

SD 3271281 7.77 34756.08 0.63 0.05 0.19 0.12 0.007 1.9 0.15 0.008

TN 31529782 10.32 417354.7 0.81 0.04 0.07 0.07 0.005 3.3 0.19 0.008

TX 1.10E+08 8.73 1442640 0.72 0.06 0.12 0.1 0.007 2.4 0.21 0.011

UT 9117265 6.69 111141.1 0.56 0.07 0.25 0.12 0.009 1.4 0.16 0.009

VA 31886894 8 401657.3 0.67 0.07 0.14 0.1 0.012 2.1 0.16 0.01

VT 2941828 8.95 20672.3 0.75 0.04 0.09 0.1 0.007 2.6 0.18 0.006

WA 34360333 9.48 430968.9 0.67 0.06 0.13 0.13 0.008 2.5 0.14 0.014

WI 18978468 6.6 198468.4 0.66 0.07 0.16 0.1 0.01 1.7 0.12 0.007

WV 3986776 5.21 34785.45 0.75 0.07 0.1 0.07 0.009 1.5 0.12 0.004

WY 2490396 9.11 36828.82 0.59 0.05 0.17 0.17 0.01 1.9 0.16 0.01