By Kent Smetters

This past Friday, Dr. Kevin Hassett, Chairman of the Council of Economic Advisers, critiqued Penn Wharton Budget Model’s analysis of the “Tax Cuts and Jobs Act” (TCJA), signed into law by President Trump in December 2017. Dr. Hassett delivered his remarks at the 2019 American Economic Association meeting. The AEA meeting is the largest annual event of academic and government economists, held this year in Atlanta, Georgia.

As background, prior to the formulation of the TCJA legislation, PWBM released its tax reform simulator in Fall 2016, with several updates thereafter. In October 2017, PWBM released its tax reform options guide for lawmakers. Between October 2017 and December 2017, PWBM released multiple projections of actual bills and amendments as they worked through the House and Senate. PWBM then released its analysis of the final (conference-committee) TCJA legislation on December 17, 2017, followed by additional studies, including the projected impact of the TCJA by industry. The experts at the Joint Committee on Taxation released their dynamic analysis of the TCJA on December 22, 2017. The White House has not previously released its own estimate of the impact of the TCJA on the budget or the economy. Instead, the White House has focused on the short-run economic impact of two changes to the tax code that impact some businesses, in particular, a corporate tax rate cut and full expensing of some investments. In contrast, the TCJA contains numerous temporary and permanent provisions, including several key business tax changes as well as changes to the individual tax code.

Figure 1 comes from Dr. Hassett’s presentation. In his remarks, Dr. Hassett claims that PWBM projected that the TCJA would increase GDP in 2018 by just 0.03 to 0.08 percentage points. Dr. Hassett also claims that PWBM’s analysis assumes that the economy is 75 percent closed, such that only 25 cents of each dollar of additional federal debt produced by the TCJA is purchased by foreign entities. Dr. Hassett argues that a larger foreign take-up of debt is more likely, thereby mitigating the negative effects of additional debt on the domestic capital stock. Dr. Hassett also argues that recent changes in oil prices did not have a significant effect on investment and GDP in 2018.

Figure 1: White House's Incorrect Characterization of PWBM Analysis

We appreciate the White House’s continued attention to PWBM’s research. Its characterization of PWBM’s projections and framework, however, is incorrect.

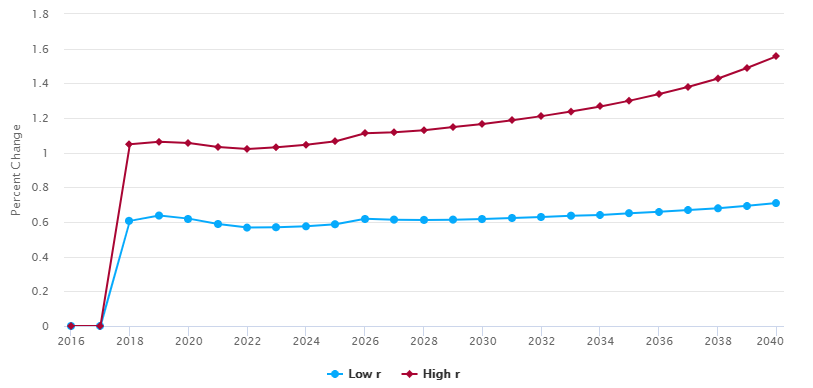

In December 2017, PWBM projected that the TCJA would produce additional GDP growth in 2018 at a value twenty times larger than stated by Dr. Hassett. Figure 2 shows that, in December 2017, PWBM projected an additional GDP growth rate of between 0.61 and 1.05 percentage points for 2018. PWBM presented these results in numerous public outlets, including at the National Bureau of Economic Research and The Brookings Institution.

Figure 2: U.S. Gross Domestic Product (GDP)

Percent Change from Current Law

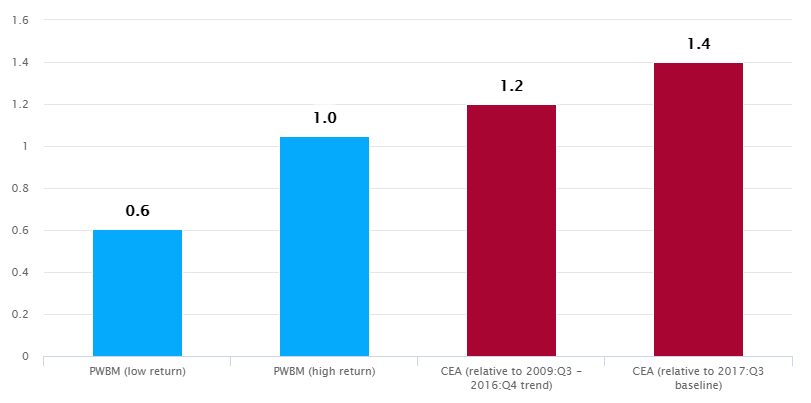

Figure 3 shows a corrected version of the chart from Dr. Hassett’s presentation, comparing PWBM’s December 2017 projection with the White House’s estimatess of the TCJA’s effect on GDP growth in 2018.

Figure 3: Effect of TCJA on GDP growth in 2018 (Corrected version of Figure 1)

Percentage points

Moreover, PWBM’s analysis does not assume a 75 percent closed economy. In our baseline estimates, PWBM assumes that 40 cents of each new dollar of debt will be purchased by foreigners, consistent with the empirical evidence, as we have previously documented. (In fact, we have previously shown that recent concerns about a trade war might make a 40-percent foreign take-up rate optimistic.) This assumption is clearly stated throughout our analysis, including with every table incorporating dynamic effects (Tables 2, 3 and 4) that we presented in our original analysis of the TCJA.

In a previous blog entry, I corrected the White House’s claim that PWBM’s model was a fully closed economy. As also noted in that blog entry, PWBM is the only entity---governmental or non-governmental---which conducts dynamic analysis of the federal budget and shows all of its major model equations and methods online. We are happy to discuss our model with White House staff at their convenience.

Finally, in his presentation last Friday, Dr. Hassett dismissed the impact of changes in oil prices in 2018 on new capital investment, instead tying the increase in investment to the TCJA. Shortly, we will release a blog post showing that changes in oil prices have had a major impact on investment in 2018.

Year,Low r,High r 2016,0,0 2017,0,0 2018,0.606463011,1.048246838 2019,0.637241018,1.062537025 2020,0.619501824,1.056311761 2021,0.58839224,1.032739884 2022,0.567658943,1.021760384 2023,0.569907465,1.030942007 2024,0.575052181,1.045645047 2025,0.587113138,1.066349051 2026,0.618888804,1.112177355 2027,0.613691165,1.117755918 2028,0.61197428,1.12939423 2029,0.613697972,1.147621043 2030,0.617120705,1.165885304 2031,0.623339394,1.187517806 2032,0.628445948,1.210849568 2033,0.636323411,1.237033386 2034,0.640387733,1.26677408 2035,0.651054084,1.300163143 2036,0.659001124,1.338324452 2037,0.669308887,1.380334707 2038,0.679078304,1.428164973 2039,0.694044315,1.489867197 2040,0.709207558,1.557351572