By John Ricco and Richard Prisinzano

Senator Kamala Harris recently announced a proposal to establish a new refundable tax credit. This proposal (henceforth referred to as the “LIFT credit”) would be similar in design to the existing Earned Income Tax Credit (EITC), providing large payments -- up to $6,000 annually for married filers -- to low- and middle-income households. The LIFT credit would be available to households with either labor earnings or Pell grants, and would offer an option to receive benefit payments monthly rather than yearly. PWBM’s preliminary analysis suggests that on a conventional scoring basis, this policy would cost nearly $3.1 trillion over the ten-year budget window (2019-2028), and would substantially change effective marginal tax rates for certain households.

While there is no specific legislative language for the proposal (hence, why our analysis is “preliminary”), some media outlets and think tanks have provided enough detail that a preliminary score is possible.1 The LIFT credit would match earnings, including Pell grants, up to $3000 ($6000) for single (married) filers. The credit would begin to phase out at $30,000 ($60,000) of income at a rate of 15 cents for every additional dollar. For single earners with children, the credit begins to phase out at $80,000. One way in which this credit differs from the EITC is that while its phase-out range depends on having children, the maximum credit amount is child-independent -- thus providing a larger boost to those without children. The proposal institutes a limit on investment income for eligibility, and the credit and threshold values would be indexed to inflation.

We use the PWBM’s tax microsimulation module to estimate the budgetary costs of the LIFT credit. For this analysis, we impute the nontaxable portion of Pell grants to households using data from the Department of Education. We also project that some households who do not file taxes under current law would now elect to file taxes in order to claim the LIFT credit.

Table 1 shows the estimated budgetary effects of the LIFT credit through 2038. We expect the proposal would cost the federal government approximately $3.1 trillion over the ten-year budget window and an additional $3.7 trillion over the following decade.

| Budget window | Out-years | |||

|---|---|---|---|---|

| Year | Budget cost | Year | Budget cost | |

| 2019 | -220.7 | 2029 | -345.2 | |

| 2020 | -290.2 | 2030 | -354.0 | |

| 2021 | -295.7 | 2031 | -357.2 | |

| 2022 | -301.4 | 2032 | -365.6 | |

| 2023 | -307.0 | 2033 | -370.1 | |

| 2024 | -316.9 | 2034 | -377.6 | |

| 2025 | -323.0 | 2035 | -381.4 | |

| 2026 | -327.9 | 2036 | -390.4 | |

| 2027 | -336.0 | 2037 | -396.3 | |

| 2028 | -340.7 | 2038 | -403.2 | |

| 2019-2028 | -3059.7 | 2029-2038 | -3741.0 | |

Note: Budget cost includes both reduced revenues and increased outlays from the refundable portion of the LIFT credit.

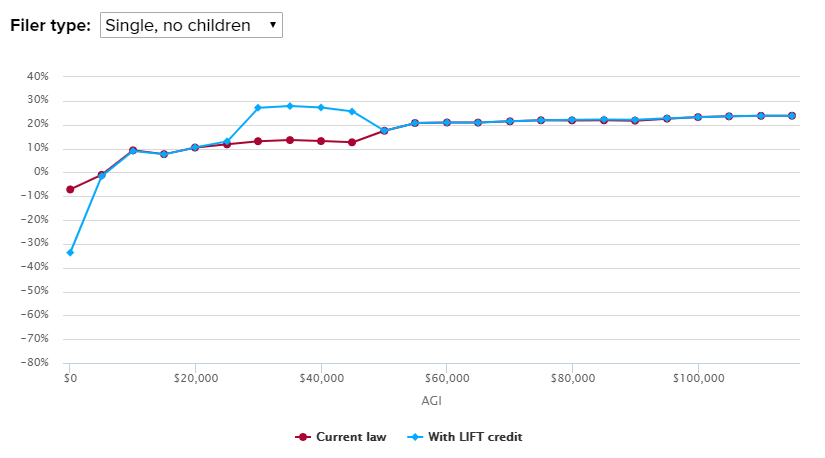

The LIFT credit would also alter effective marginal rates on labor earnings. For every additional dollar that filers earn up to $3,000 ($6,000 for married filers), the value of the LIFT credit increases by one dollar. This implies an effective marginal tax rate of negative 100 percent. For households in the phase-out range, each additional dollar of earnings is met with a 15 cent reduction in the value of the LIFT credit, implying an extra 15 percent marginal tax rate on top of existing marginal rates. These changes may influence household choices about whether to work, and if so, how many hours to work. Evidence from the EITC suggests that the phase-in may encourage low-income non-workers to enter the labor market, and a large body of research measuring labor supply elasticities indicates that the LIFT credit’s phase-out range may modestly reduce work incentives. Figure 1 shows effective marginal tax rates on wage earnings for different types of filers under current law and Senator Harris’s proposed credit. Choose from the drop down menu to view plots for married filers, single filers with children, and single filers without children.

Note: Effective marginal rates reflect the individual income tax only. Calculations include current law tax filers only.

This analysis is incomplete without additional details from Senator Harris. For instance, Senator Harris has expressed interest in repealing elements of the Tax Cuts and Jobs Act---particularly provisions benefitting high-income households---to pay for some or all of the cost of the LIFT credit. With more details, PWBM would be able to conduct a dynamic analysis of the proposal using the full capabilities of our model and show macroeconomic feedback effects.

-

See: The Atlantic, Tax Policy Center and Tax Foundation. ↩