By Austin Herrick

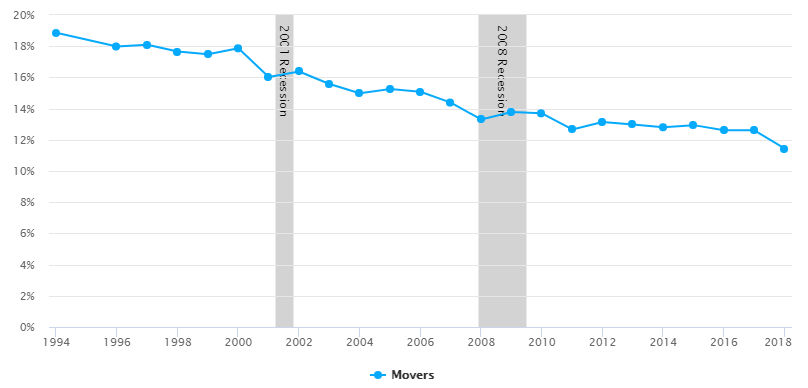

Internal migration of working-age people in the United States has fallen by more than a third – from 18.86 percent in 1994 to 11.44 percent in 2018 (see Figure 1). This phenomenon has received significant scholarly attention – Cooke (2013)1 for example, attributes this decline to the rise of information and communication technologies. Alternatively, Molloy, Smith, and Wozniak (2011)2 point to broad macroeconomic shifts.

Reduced internal migration has important economic implications, particularly for labor markets. We find that wages grow faster for movers, especially for those with a college degree.

Source: Current Population Survey (1994 – 2018)

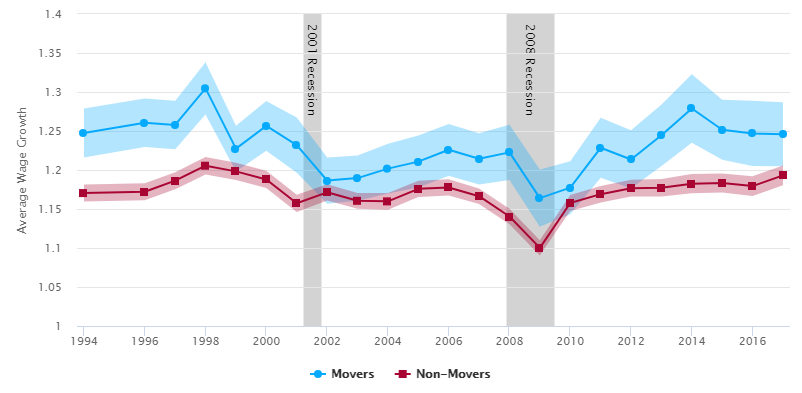

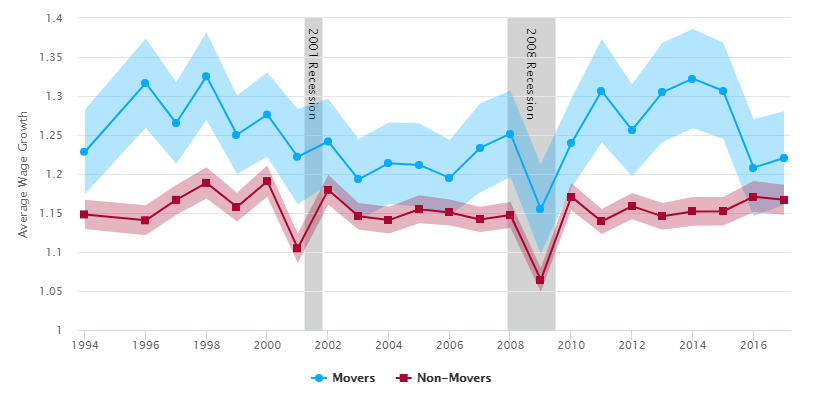

Figure 2 below shows observed wage growth for movers and non-movers over the last twenty years. As seen by the difference between the red and blue solid lines, the wage premium3 for moving over the last two decades has remained relatively constant, despite recessions (shaded gray) during the intervening years. The wage premium for moving suggests that migration improves matching between employers and employees.

Note: The shaded blue and red ares represent 95 percent confidence intervals.

Source: Current Population Survey (1994 – 2018)

We might expect declines in migration to be correlated with changes in the labor market. As labor markets weaken, the wage premium for movers may decrease. Firms may be less willing to pay a premium to attract new workers in an economy where many current workers are being laid off.

The available data has some limitations. We only observe movement behavior of individuals who make the decision to move, which fewer people did in the wake of the financial crises in 2001 and 2008. It is possible that the wage premium for moving for all workers has decreased over time, even as the marginal wage premium for moving has remained steady. That is, given fixed costs of moving, workers offered lower wage premiums for moving decided against movement altogether, biasing upward the average wage premium for moving. The premium’s increase in recent years indicates labor markets seeking new talent in a population of households still wary about movement.

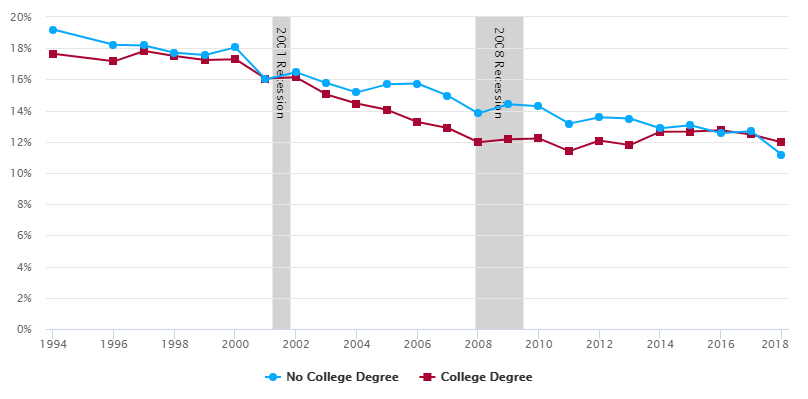

This suggested pattern of firms searching for new movers becomes more plausible when examining movement patterns of adults based on educational attainment. In Figure 3, we see that the movement rate for college-educated adults fell significantly faster than their non-college educated peers beginning in the early 2000s. Interestingly, this decline stabilizes around 2011.

Source: Current Population Survey (1994 – 2018)

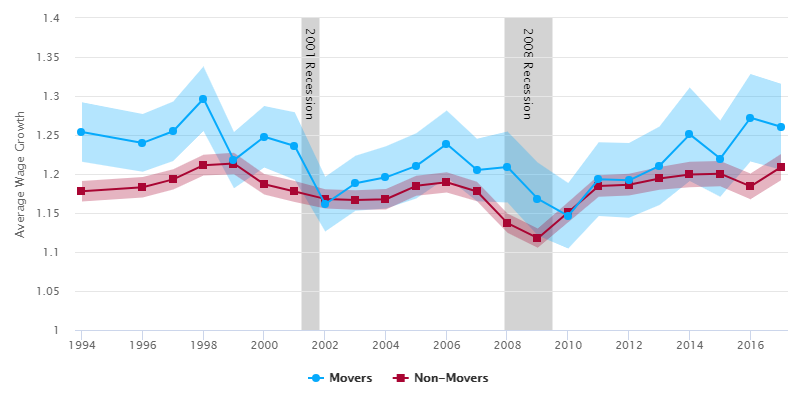

Further evidence of education’s effect on movement is shown in Figures 4 and 5, which display the wage premium of movers, conditioned on college degree attainment. From Figure 4, we see that the movement premium for non-college educated workers is often not statistically significantly above 0. Companies seem relatively unwilling to offer these less-educated workers a significant premium to induce movement, largely independent of economic conditions.

Note: The shaded blue and red ares represent 95 percent confidence intervals.

Source: Current Population Survey (1994 – 2018)

By contrast, in Figure 5, we see a highly significant wage premium for moving offered to college-educated workers. The data seems to reflect that college-educated workers are the primary recipients of the observed wage premium for movers.

This conclusion matches the results found by Gould (2007).4 In that study, Gould finds that higher urban wages are primarily driven by white-collar workers (a rough proxy for college education). Critically, the leveling-off of the college educated movement rate observed around 2011 maps onto the significant increase in the wage premium for moving observed for these workers in Figure 5. This observation supports the conclusion that wage premiums are successful in inducing movement.

Note: The shaded blue and red ares represent 95 percent confidence intervals.

Source: Current Population Survey (1994 – 2018)

We’ve identified that the wage premium for moving influences the decision to move. However, declining premiums only explain some of the puzzle - increasing premiums only stabilize, rather than reverse, internal migration rates, and movement has fallen dramatically over the past two decades. This suggests significant non-labor market factors affecting movement for American workers. We know the decision to move is influenced by the cost of moving and housing, among other things. A forthcoming post will explore the reasons why people report that they move.

-

Cooke, T. J. (2013). Internal Migration in Decline, The Professional Geographer, 65(4), 664-675. doi:10.1080/00330124.2012.724343 ↩

-

Molloy, R., Smith, C. L., & Wozniak, A. (2011). Internal Migration in the United States, Journal of Economic Perspectives, 25(3), 173-96. ↩

-

The wage premium measures the ratio of wage increases for individuals who moved compared to non-movers. For example, if the average non-mover received a 2 percent raise, compared to a 3 percent raise for movers, the wage premium is 50 percent. ↩

-

Gould, E. D. (2007). Cities, Workers, and Wages: A Structural Analysis of the Urban Wage Premium, The Review of Economic Studies, 74(2), 477–506. doi:10.1111/j.1467-937X.2007.00428.x ↩

Value,Movers,StandardError 1994,18.860913,0.001304 1996,17.981096,0.001375 1997,18.09522,0.001368 1998,17.65817,0.001354 1999,17.486219,0.001343 2000,17.864216,0.001343 2001,16.023391,0.001019 2002,16.378894,0.001029 2003,15.574425,0.001008 2004,14.979454,0.000998 2005,15.25065,0.001013 2006,15.07861,0.001011 2007,14.386101,0.000995 2008,13.302812,0.000962 2009,13.777376,0.000972 2010,13.695174,0.000964 2011,12.661716,0.000941 2012,13.142633,0.000966 2013,12.98464,0.000961 2014,12.803088,0.000964 2015,12.940293,0.000971 2016,12.613803,0.000997 2017,12.608216,0.000997 2018,11.439719,0.000974

Value,Movers,StandardError,Non-Movers,StandardError 1994,1.247495,0.016035,1.170402,0.005542 1996,1.26065,0.015858,1.172045,0.005603 1997,1.257741,0.015848,1.186335,0.005552 1998,1.3047,0.017126,1.205488,0.005668 1999,1.227436,0.015016,1.198246,0.005688 2000,1.256591,0.016263,1.187875,0.005621 2001,1.231814,0.018098,1.157326,0.005665 2002,1.186505,0.015139,1.171365,0.005269 2003,1.18962,0.014831,1.160491,0.005176 2004,1.201743,0.01623,1.159778,0.005399 2005,1.210759,0.017004,1.175856,0.005332 2006,1.225942,0.016924,1.177659,0.005276 2007,1.214335,0.016724,1.166409,0.005096 2008,1.222592,0.018108,1.140365,0.005089 2009,1.163884,0.018701,1.100223,0.004951 2010,1.177334,0.017306,1.157686,0.005289 2011,1.228495,0.019639,1.16902,0.005381 2012,1.213471,0.019047,1.176732,0.005478 2013,1.244533,0.020161,1.17721,0.005727 2014,1.278861,0.022376,1.182468,0.006285 2015,1.251548,0.019592,1.183309,0.006243 2016,1.246865,0.021362,1.179344,0.0065 2017,1.245718,0.020933,1.193169,0.006493

Value,No College Degree,StandardError,College Degree,StandardError 1994,19.197801,0.001483,17.651563,0.002732 1996,18.226941,0.001571,17.158485,0.002841 1997,18.178303,0.001559,17.81851,0.002849 1998,17.708835,0.001548,17.494488,0.002793 1999,17.564441,0.001542,17.242727,0.002735 2000,18.050993,0.001546,17.294799,0.002716 2001,16.013412,0.001176,16.052715,0.00204 2002,16.46367,0.001195,16.134575,0.002026 2003,15.764783,0.001175,15.037159,0.00196 2004,15.169847,0.001166,14.450081,0.001929 2005,15.681302,0.001193,14.050111,0.001912 2006,15.735138,0.001199,13.272455,0.001865 2007,14.955941,0.001186,12.885191,0.001819 2008,13.822156,0.001151,11.978495,0.001741 2009,14.411261,0.001169,12.157264,0.001736 2010,14.277546,0.001156,12.215951,0.001736 2011,13.166185,0.001133,11.404628,0.00168 2012,13.576897,0.001165,12.081713,0.001722 2013,13.491182,0.001166,11.787578,0.00169 2014,12.868659,0.001156,12.650868,0.001746 2015,13.066364,0.001167,12.653443,0.00175 2016,12.557117,0.001195,12.738154,0.001809 2017,12.673547,0.001206,12.468703,0.001772 2018,11.17868,0.001171,11.969263,0.001752

Value,Movers,StandardError,Non-Movers,StandardError 1994,1.253834,0.019427,1.177749,0.006713 1996,1.239843,0.018857,1.182977,0.006746 1997,1.254741,0.019438,1.193117,0.006695 1998,1.296529,0.021148,1.211375,0.006786 1999,1.217764,0.018452,1.213427,0.007005 2000,1.247774,0.020068,1.186785,0.00671 2001,1.235923,0.022139,1.177596,0.006926 2002,1.161341,0.017927,1.168079,0.006246 2003,1.188094,0.01795,1.166584,0.0064 2004,1.195718,0.020412,1.167584,0.006754 2005,1.210386,0.021383,1.184845,0.006551 2006,1.238538,0.021908,1.189329,0.006654 2007,1.205087,0.020417,1.177595,0.006408 2008,1.208936,0.023265,1.137078,0.00634 2009,1.168033,0.0239,1.117678,0.006307 2010,1.146471,0.021458,1.151063,0.006643 2011,1.193423,0.024071,1.184501,0.007009 2012,1.191912,0.024475,1.186343,0.007081 2013,1.210524,0.025662,1.194348,0.007481 2014,1.250835,0.030568,1.199435,0.008345 2015,1.219794,0.024938,1.200393,0.008242 2016,1.272122,0.028625,1.184169,0.00838 2017,1.260586,0.028073,1.208867,0.008574

Value,Movers,StandardError,Non-Movers,StandardError 1994,1.228554,0.027638,1.148219,0.009518 1996,1.316511,0.029156,1.140625,0.009818 1997,1.26534,0.026775,1.166892,0.009743 1998,1.325323,0.028698,1.188617,0.010188 1999,1.250309,0.025628,1.157595,0.009452 2000,1.276157,0.027601,1.190844,0.010249 2001,1.222138,0.031195,1.104865,0.009633 2002,1.24169,0.027941,1.179674,0.009816 2003,1.193132,0.026362,1.145974,0.008672 2004,1.213804,0.026622,1.140915,0.008791 2005,1.21167,0.027175,1.15486,0.009105 2006,1.195057,0.024828,1.150662,0.008444 2007,1.233377,0.029148,1.141698,0.008258 2008,1.251646,0.028301,1.147409,0.008507 2009,1.155006,0.029246,1.064293,0.007808 2010,1.239162,0.029182,1.171014,0.008724 2011,1.30665,0.033848,1.139119,0.008189 2012,1.256258,0.030063,1.158842,0.008559 2013,1.304719,0.032466,1.145737,0.008737 2014,1.322299,0.032442,1.151953,0.009393 2015,1.306671,0.031608,1.152218,0.009316 2016,1.208228,0.031711,1.170972,0.010243 2017,1.220534,0.030614,1.166938,0.009826