Key Points

We project that the Tax Cuts and Jobs Act (TCJA) will cause 235,780 U.S. business owners---77 percent of whom have incomes of at least $500,000---to switch from pass-through entity owners to C-corporations, primarily to take advantage of sheltering their income from tax by converting to C-corporations.

The biggest switchers include doctors, lawyers and investors, especially if owners can afford to defer receipt of business income to a later year. Other business owners, who are qualified to use the 20 percent deduction for pass-through business income, including painters, plumbers, and printers, are more likely to remain as pass-through entities.

We project that about 17.5 percent of all pass-through Ordinary Business Income will switch to C-corporations.

Summary

We project that the recent tax act will cause at least 235,780 individual business owners to switch from owners of pass-through entities to C-corporations, representing about 17.5 percent of Ordinary Business Income from pass-throughs.

Projecting the Mass Conversion from Pass-Through Entities to C-Corporations

Introduction

The Tax Cuts and Job Act (TCJA), which came into effect on January 1, 2018, lowers the corporate tax rate from a top rate of 35 percent to a rate of 21 percent. As a result, earlier this year, two prominent private equity firms, Ares and KKR, converted from a partnership to a C-corporation. Other firms, especially service firms with high income owners who do not have access to the new law’s 20 percent deduction for pass-through income, are also considering the same move.

Penn Wharton Budget Model (PWBM) previously reported both the static and dynamic effects of the TCJA as well as the effective tax rates by industry before and after passage of the bill. The TCJA changed the relative tax rates faced by pass-through businesses (S-corporations, partnerships and sole proprietorships) and C-corporations. Our previous analyses of the TCJA include this type of income shifting and reclassification at the macroeconomics level, and we previously reported the methods we used to make our estimates.

This brief reports the number and types of businesses that benefit the most under the new tax law and are, therefore, mostly likely to change their form of organization. Business owners can use a simplified version of PWBM’s tax module to compare average tax rates as a C-corporation versus a pass-through entity. The calculations presented in this brief use the full power of PWBM’s tax module.

The Taxation of Business Income

Pass-through businesses and C-corporations are taxed differently. Pass-through business income is taxed only at the owner level,1 whereas C-corporate income is taxed first at the corporate level and then again at the owner level when profits are distributed.

Prior to the passage of the TCJA, C-corporate income faced a combined corporate and owner tax rate which was often higher than the tax rate faced by pass-through business income. Therefore, prior to the passage of the TCJA, the U.S. tax code encouraged certain businesses to prefer pass-through form over C-corporate form. Indeed, pass-through businesses became increasingly prominent over time. In 1980, 17 percent of businesses were C-corporations. But, by 2013, only 5 percent of businesses were C-corporations. Similarly, C-corporations accounted for 79 percent of business income in 1980 but only 50 percent in 2013.2 The increasing importance of pass-through businesses has been attributed to changes in liability laws,3 differential treatment of wages and profits,4 and the disparity in taxation of business income.5 It is the latter explanation that we explore in this brief.

The TCJA introduced a provision known as Section 199A which allows certain owners of pass-through businesses to deduct up to 20 percent of qualified business income from their overall taxable income.6 Many lawyers and economists have noted the potential tax arbitrage opportunities that Section 199A presents. In particular, the TCJA provides strong incentives for businesses to either convert to a C-corporation or recharacterize income received by businesses limited under the provision.7 Other papers have presented examples of the tax faced by business income received by different tax units under alternative organizational forms.8

This brief adds to the growing body of research surrounding business entity choice under the TCJA. The advantage of our analysis is that we use PWBM’s tax module---which is calibrated to IRS microdata---rather than simple examples to model business organizational decisions. For each simulated tax unit with pass-through income, we are able to calculate the average tax rate on pass-through income before and after the passage of the TCJA and then estimate the average rate if they instead organized as C-corporations. We also present breakdowns based on pass-through type and under different scenarios where firms are able to retain earnings to benefit from tax deferral. Taken as a whole, this brief presents a more detailed picture of which kinds of businesses have the greatest tax incentives to reorganize under the TCJA.

TCJA Changes Incentives to Organize as C-Corporation

The TCJA produces significant tax savings for many pass-through businesses to reorganize as C-corporations. The process of reorganizing for tax purposes is largely costless since the introduction of the ‘check the box’ elections in 1996.

The TCJA changed both the corporate and individual rates, so that there is now little difference between the tax rates paid on C-corporate and pass-through business income. For example, Table 1 shows that in 2017, C-corporate income faced a top tax rate that was 7.1 percentage points higher than the top tax rate faced by pass-through business income. In 2018, the top tax rate faced by C-corporate income is actually 1 percentage point lower. In 2018, under the TCJA, some pass-through businesses qualify for a deduction of 20 percent which lowers the top marginal rate on pass-through business income to 29.6 percent.9 The difference between net tax rates on C-corporations and pass-through businesses is larger (6.4 percent) for pass-through businesses that qualify for the deduction, but still less than in 2017. This change in relative tax rates may make organizing as a C-corporation more appealing, particularly if a business’s marginal rate is considerably lower than the statutory tax rate or the individual owner faces a lower individual tax rate on qualified dividends and/or long-term capital gains.

| 0% Retained Earnings | |||||

|---|---|---|---|---|---|

| 2017 | 2018 | ||||

| Type of Tax | C-Corporation | Pass-through | C-Corporation | Pass-Through | with 20% Deduction |

| Entity Tax | 35.0% | 0.0% | 21.0% | 0.0% | 0.0% |

| Individual Tax | 20.0% | 39.6% | 20.0% | 37.0% | 29.6% |

| Net Investment Income Tax | 3.8% | 3.8% | 3.8% | 3.8% | 3.8% |

| Net Rate | 50.5% | 43.4% | 39.8% | 40.8% | 33.4% |

| Rate Differential | 7.1 | -1.0 | 6.4 | ||

| 100% Retained Earnings | |||||

| 2017 | 2018 | ||||

| Entity Tax | 35.0% | 0.0% | 21.0% | 0.0% | 0.0% |

| Individual Tax | 0.0% | 39.6% | 0.0% | 37.0% | 29.6% |

| Net Investment Income Tax | 0.0% | 3.8% | 0.0% | 3.8% | 3.8% |

| Net Rate | 35.0% | 43.4% | 21.0% | 40.8% | 33.4% |

| Rate Differential | -8.4 | -19.8 | -12.4 | ||

Calculating the Tax Rates for Different Types of Businesses

Under the U.S. tax code, C-corporate profits are taxed once at the entity level and then again at the individual level as either a dividend or capital gain. It is important to consider both layers of taxation in analyzing the costs and benefits of C-corporation status. It is also important to consider the fact that an owner of a C-corporation can retain any or all of the profits in the corporation and defer taxation. Therefore, the rate faced by C-corporate income is a function of the corporate rate, the dividend rate, the capital gains rate and the benefit from retained earnings as illustrated in equation 1:

Here, τnc is the net corporate rate, cis the statutory corporate rate, τc the tax rate of dividend income, τcg is the tax rate on capital gains income, α is the share of corporate income paid out as dividends and β is a measure of the benefits to capital gains deferral.10

Retaining earnings in a corporation is a benefit to C-corporate form. Pass-through businesses by definition do not allow retained earnings; all income passes through to the owner and is taxed in the year it is earned. Our analysis considers three scenarios for retained earnings: No retained earnings (all income is paid out in the year it is earned), 100 percent retained earnings (no income is paid out in the year it is earned) and 52 percent retained earnings (the average dividend payout rate from 1959-2015).

We follow the methodology set forth by Cooper et al., (2015) to assign a tax rate to types of income allocated from specific pass-through entities. Data limitations do not allow identification of the type of income from specific types of entities other than Ordinary Business Income (OBI), which is a business’ main source of income, which is derived from normal operations of a business.11 Unidentified income includes capital gains, dividends and interest. However, both capital gains and qualified dividends already face the lowest possible rate (0 percent/15 percent/20 percent) if received through a pass-through business and, therefore, would not benefit from conversion. Moreover, interest income and ordinary dividends face ordinary rates, and so conversion may lower the tax rate faced by this income. But, this type of income can’t be identified from the available data.

We consider the total dollar amounts of partnership, sole proprietorship and S-corporation OBI as eligible for conversion to a C-corporation. The income earned by a single member LLC or sole proprietorship is easy to convert to C-corporate income since there are no partners to consider. Since a partner’s taxation is independent of the other partners in the partnership and a partner can be either an individual or an entity, a partner can convert their own income to corporate form. In the case of S-corporations, the conversion to C-corporation is more complicated since multiple individuals can be shareholders of S-corporations and any conversion requires the agreement of each shareholder. However, the average S-corporation only has 1.7 shareholders and are by definition closely held. Additionally, it is likely that each shareholder faces similar rates. As such, we consider each S-corporation shareholder as the lead owner and therefore, able to make the conversion decision and consider the OBI earned as eligible for conversion.12

For each type of pass-through business, we subject OBI from that type of business to the corporate tax structure in place prior to January 1, 2018. We also subject a portion of the after tax profits to the relevant dividend rate faced by the individual owner. The portion subjected to the dividend tax is determined by the three retained earnings scenarios mentioned above.

To estimate the firms that switch from pass-through to C-corporation, we need to correct for the fact that some business owners were failing to minimize taxes prior to the passage of the TCJA. Toward that end, for each business owner, we first calculate a tax rate differential between the ‘net corporate rate’ (both layers of tax) and the individual rate as a pass-through entity before the passage of the TCJA (the “pre-TCJA tax rate differential”). Similarly, we calculate a tax rate differential between the ‘net corporate rate’ (both layers of tax) and the individual rate as a pass-through entity after the passage of the TCJA (the “post-TCJA tax rate differential”). We assume that business owners for whom the pre-TCJA tax rate differential was negative (i.e., these business owners failed to minimize taxes) do not switch entity types. Business owners, for whom the pre-TCJA tax rate differential was positive and the post-TCJA tax rate differential is negative, are then assumed to switch.

Pass-Through Business Income is Concentrated Among High Earners

Cooper et al. (2015) noted that pass-through business income in 2010 was concentrated among high earners. Because of this concentration, most pass-through business income is subject to the highest marginal tax rates in the individual income tax code and likely not able to use the new pass-through deduction.

This finding is reflected in Table 2. Income from pass-through businesses is largely received by tax units with Adjusted Gross Income (AGI) above $100,000. Filers above this AGI cutoff receive over 90 percent of partnership and S-corporation OBI and over 50 percent of sole proprietorship OBI. On average, these filers receive just over $160,000 of partnership OBI, just over $200,000 of S-corporation OBI and just under $51,000 of sole proprietorship OBI.

Pass-through type

| With partnership income (Billions of $) | With S-corporation income (Billions of $) | With sole proprietership income (Billions of $) | |||||||

|---|---|---|---|---|---|---|---|---|---|

| AGI | Number of Returns | Partnership OBI | AGI | Number of Returns | S-corporation OBI | AGI | Number of Returns | Sole proprietership OBI | AGI |

| $0 or negative | 58,046 | $4 | -$29 | 78,617 | $6 | -$29 | 351,288 | $5 | -$41 |

| $0-$100K | 1,201,380 | $20 | $61 | 1,417,118 | $34 | $76 | 13,131,504 | $176 | $473 |

| $100K-$250K | 1,025,626 | $40 | $162 | 1,244,574 | $69 | $194 | 3,321,428 | $104 | $488 |

| $250K-$500K | 446,157 | $55 | $157 | 442,246 | $63 | $153 | 656,999 | $58 | $220 |

| $500K-$1M | 246,182 | $62 | $170 | 203,146 | $59 | $140 | 163,829 | $26 | $110 |

| $1M-$2.5M | 118,849 | $64 | $177 | 101,777 | $72 | $151 | 59,026 | $15 | $86 |

| $2.5M+ | 42,771 | $83 | $308 | 39,809 | $146 | $307 | 16,732 | $10 | $117 |

The Incentive for Business Reorganization

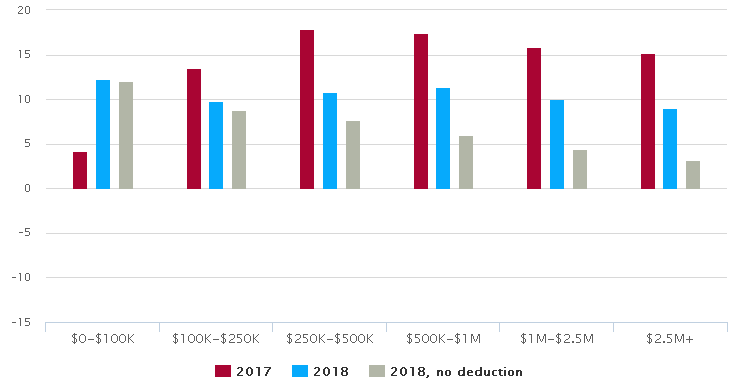

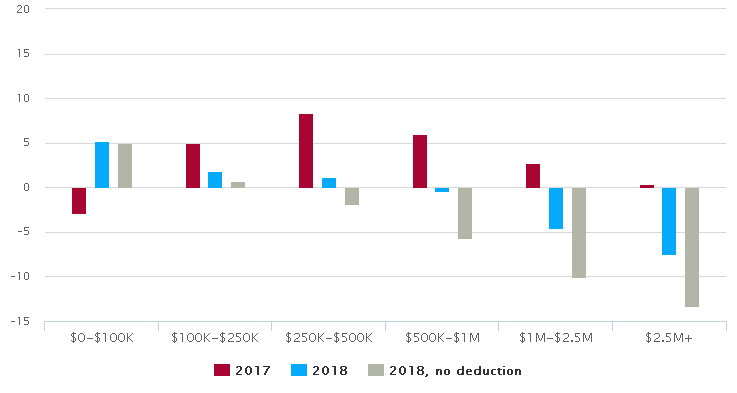

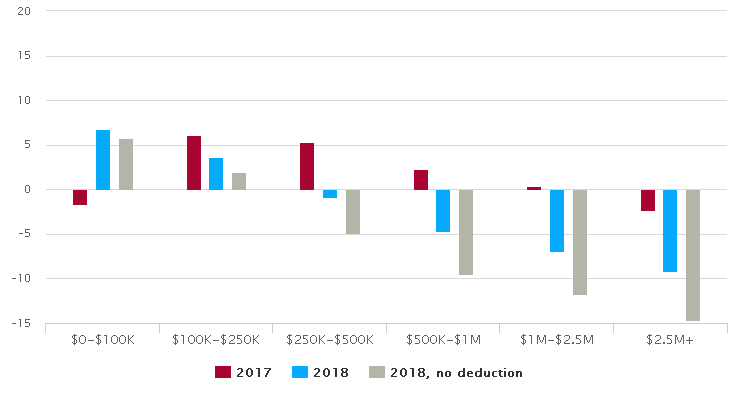

Figure 1 presents the results of the tax experiment where all after tax income is distributed as qualified dividends to the individual owner. Use the drop down box to select results for partnership, S-corporation and sole proprietorship OBI. For each AGI class, the rate differential is highest in 2017, under pre-TCJA law, (red column) since the reduction of the corporate rate is larger than the reduction of the individual rates. The lone exception is the lowest AGI class which is hurt by the elimination of the graduated corporate rates present in the 2017 tax code. The blue columns represent the average rate differential in 2018, under the new tax code. The fact that the average differential is smaller in 2018 indicates that the incentive to file taxes as a pass-through business is smaller than in 2017. The grey column represents the average rate differential if there were no deduction for pass-through income in 2018 under the new tax code. This column coarsely represents the group of filers whose deduction is limited by either income or business type. These differentials suggest that businesses that are unable to use the pass-through deduction face less of an incentive to file taxes as a pass-through business.

Pass-through type

Partnership

S-Corporation

Sole Proprietorship

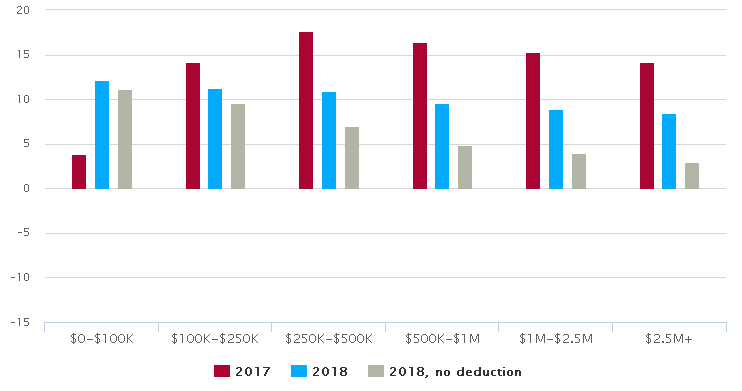

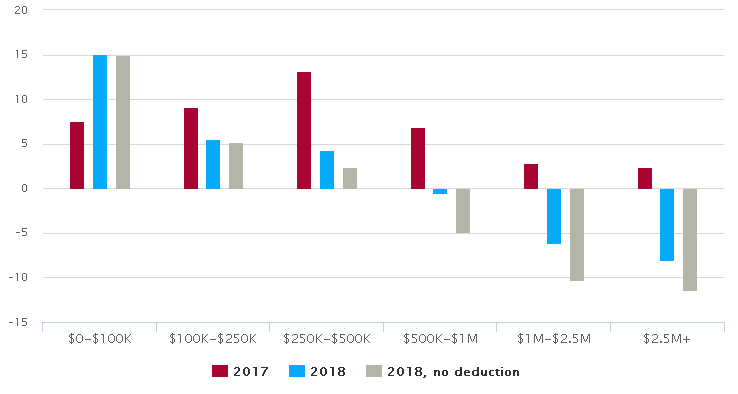

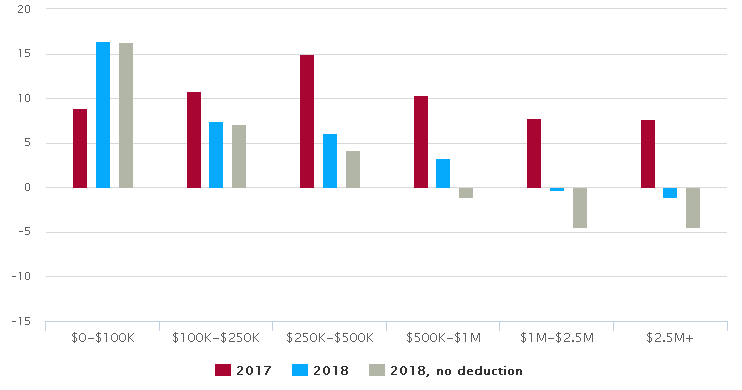

Figure 2 presents the average rate differentials by AGI class for the experiment where no after tax income is distributed as dividends to individual owners. Under this experiment, it is clear that tax units with more than $500,000 in AGI benefit from filing taxes as a C-corporation since the rate differential is actually negative no matter the type of pass-through business. However, for S-corporation OBI, the benefit to filing as a C-corporation is clear for tax units with more than $250,000 in AGI.

Pass-through type

Partnership

S-Corporation

Sole Proprietorship

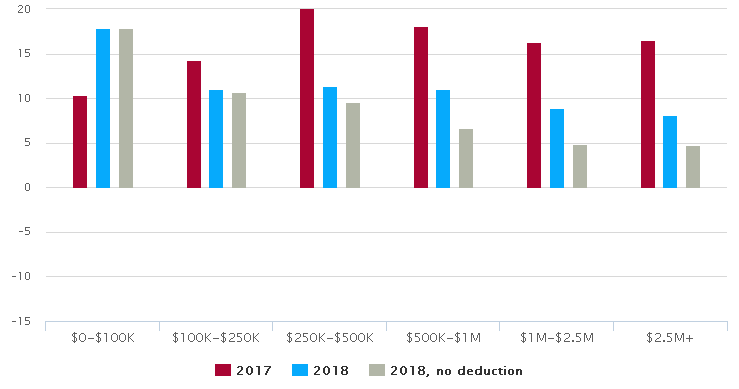

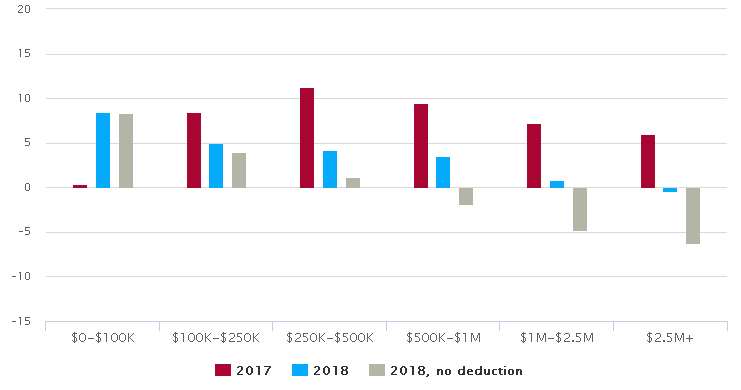

Figure 3 presents the average rate differentials by AGI class for the experiment where an ‘average’ amount of income is retained in the C-corporation (52 percent). Tax units with more than $2,500,000 in AGI clearly benefit from filing taxes as a C-corporation for those units with Partnership OBI while for S-corporations and sole proprietorships, that cutoff is $1,000,000 in AGI.

Pass-through type

Partnership

S-Corporation

Sole Proprietorship

Number of Business who Benefit from Reorganization

Who benefits from reorganization depends on the particular circumstances of individual filers. Namely, the type of business they operate, their total taxable income and their willingness to defer income. The clear beneficiaries are those for which the difference between the net corporate rate and the pass-through rate was positive under old tax law and is negative under new tax law. We find that if owners of pass-through businesses defer 52 percent of their after tax income from the pass-through businesses, 235,780 of the 24.4 million business owners clearly benefit from reorganization.13 The group that benefits from reorganization is largely high income filers with 77 percent receiving at least $500,000 in AGI. This result is reflective of the ability of high income filers to defer income and the income limitations on the 20 percent deduction. It may also reflect the fact that high income earners are more likely to have income from businesses that are disallowed from the 20 percent deduction.

Conclusion

Prior to the TCJA, pass-through businesses were growing remarkably over time. We project that the TCJA will reverse this trend. In particular, we project that 235,780 individual business owners---especially higher income business owners or service providers---will switch from owners of pass-through entities to C-corporations, representing about 17.5 percent of Ordinary Business Income from pass-throughs.

Business owners can use a simplified version of PWBM’s tax module to compare average tax rates as a C-corporation versus a pass-through entity.

[Updated 6/13/2018 to include additional information about methodology and net tax rates.]

-

In the case of partners in partnerships that are C-corporations, the income is taxed at the corporate level and would therefore, be taxed twice. ↩

-

Author’s calculations using SOI-IRS data. This pattern has been noted by DeBacker, Jason, and Richard Prisinzano. “The Rise of Partnerships.” Tax Notes 147, no. 13 (2015); Prisinzano, Richard, Jason DeBacker, Jason, John Kitchen, Matthew Knittel, Susan Nelson, and James Pearce. “Methodology to Identify Small Businesses,” n.d., 27; and Nelson, Susan C. “Paying Themselves: S Corporation Owners and Trends in S Corporation Income, 1980-2013,” 2016, 29. ↩

-

DeBacker and Prisinzano (2015) ibid. ↩

-

Nelson (2016) ibid. ↩

-

Prisinzano, Richard and James Pearce. 2018. “Tax Based Switching of Business Income.” PWBM Working Paper, no. 2018-2. Philadelphia, PA: Penn Wharton Budget Model (March). Available at http://budgetmodel.wharton.upenn.edu/papers/2018/3/16/w2018-2, Goolsbee, Austan. “Taxes, Organizational Form, and the Deadweight Loss of the Corporate Income Tax.” Journal of Public Economics, 1998; Mackie‐Mason Jeffrey K., & Gordon Roger H. (2012). How Much Do Taxes Discourage Incorporation? The Journal of Finance, 52(2), 477–506; Carroll, Robert, and David Joulfaian. “Taxes and Corporate Choice of Organizational Form,” 1997, 24; Feldstein, Martin, Louis Dicks-Mireaux, and James Poterba. “The Effective Tax Rate and the Pretax Rate of Return.” Journal of Public Economics 21, no. 2 (July 1, 1983): 129–58; Feldstein, Martin S., and Joel Slemrod. “Personal Taxation, Portfolio Choice, and the Effect of the Corporation Income Tax.” Journal of Political Economy 88, no. 5 (1980): 854–66. ↩

-

The 20 percent deduction is limited by the taxable income the filer receives ($157,500/$315,000, single/joint), the W-2 wages the business pays, and whether the business is a service business. The PWBM tax module accounts for each of these limitations. ↩

-

Kamin, David, David Gamage, Ari D. Glogower, Rebecca M. Kysar, Darien Shanske, Reuven S. Avi-Yonah, Lily L. Batchelder, et al. “The Games They Will Play: Tax Games, Roadblocks, and Glitches Under the New Legislation.” SSRN Scholarly Paper. Rochester, NY: Social Science Research Network, December 7, 2017 and Looney, Adam. “The next Tax Shelter for Wealthy Americans: C-Corporations.” Brookings (blog), November 30, 2017. ↩

-

Repetti, James R. “The Impact of the 2017 Act’s Tax Rate Changes on Choice of Entity.” SSRN Scholarly Paper. Rochester, NY: Social Science Research Network, March 5, 2018. Borden, Bradley T. “Choice-of-Entity Decisions Under the New Tax Act.” SSRN Scholarly Paper. Rochester, NY: Social Science Research Network, February 7, 2018. ↩

-

The top individual income tax rate is now 37 percent, so .37 x (1 - 0.2) = 29.6 percent. ↩

-

This methodology follows Prisinzano and Pearce (2018), Goolsbee (1998) ibid, Mackie-Mason and Gordon 2012) ibid, Carroll and Joulfaian (1997) ibid and Feldstein et al. (1983). ↩

-

This measure excludes income the business receives from capital gains, interest and qualified dividends. ↩

-

It is important to note that the income PWBM can not identify from pass-through entities includes income that faces preferential rates and therefore, faces optimal rates if received through a pass-through (0 percent/15 percent/20 percent vs. 21 percent). PWBM can not identify interest income which face ordinary rates and may face a lower rate if converted and retained in a C-corporation. ↩

-

An individual tax return may have multiple ownership shares from any individual type of pass-through entity as well as ownership shares from multiples types of pass-through entities. We consider the conversion of each type of business entity separately. As such, an individual return may be counted more than once in the calculation of business owners. ↩