By Efraim Berkovich

PWBM’s Dynamic OLG model simulates the partially-open U.S. economy in a way that is more consistent with economic behavior than standard “model blending” exercises. The difference between the two techniques becomes more pronounced over time due to the nation’s expanding debt path.

Background

The openness of the U.S. economy to foreign capital flows helps determine the path of capital growth and, thus, future GDP. If the U.S. economy were completely closed to capital flows, all government debt and productive capital would be owned, by definition, by U.S. households. In this scenario, new debt crowds out productive investment, reducing GDP.

Opening the economy implies that foreigners purchase some of capital and debt, thereby reducing crowd-out. If the United States were both a small country and fully open to international capital flow (also known as a “small open economy”), debt would have no effect on capital formation. In reality, the United States is both large and not fully open. The U.S. economy, therefore, is best described as “partially open,” where foreign flows exist but are not at the level of a fully open economy.

Two Approaches: PWBM vs. Standard “Model Blending”

PWBM's Dynamic OLG model allows for partial foreign flows on a time-varying basis (to model policies that might impact the openness over time). An alternative and fairly standard approach would be to estimate a partially-open economy through a convex combination of solutions for a closed economy and a fully open economy, which is standard with “model blending” exercises. This alternative is less costly in terms of calculations. However, under this approach, forward-looking agents are not fully aware of the restrictions on capital flows.1 Awareness of those restrictions may influence decisions to work and save, thereby affecting projections of labor, capital and GDP. Moreover, there is no reason to expect consistency between GDP as calculated from the nonlinear Cobb-Douglas production function and the inputs of capital and labor in the alternative convex estimate.

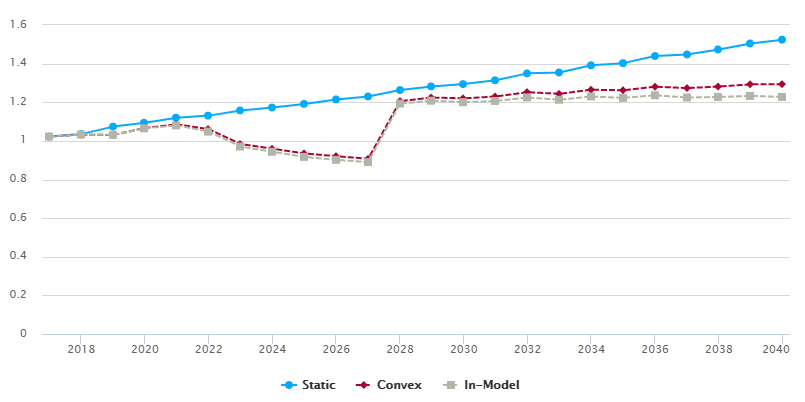

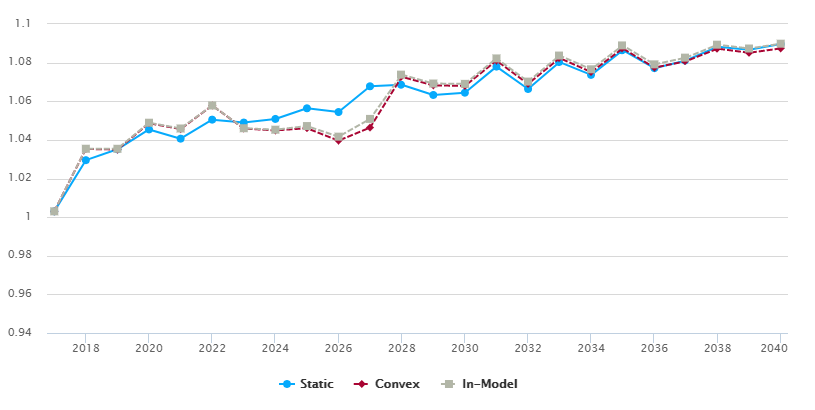

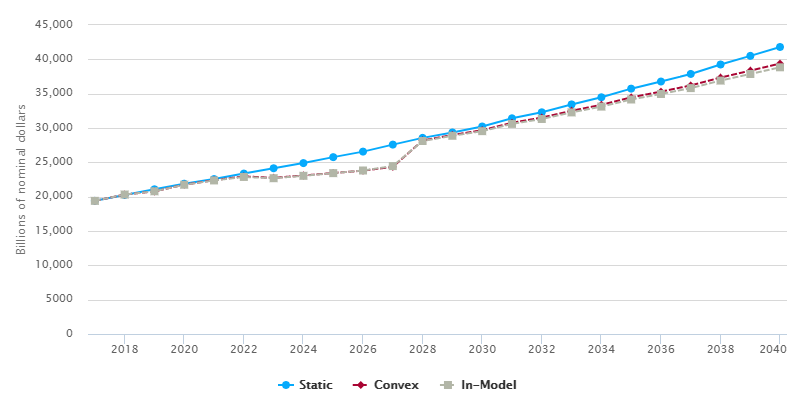

PWBM has previous documented the government’s expanding debt path under current law (see Figure 3 here). Below, Figures 1 to 3 display PWBM’s projections for future capital, labor and GDP under three scenarios. The “in-model” dynamic approach corresponds to PWBM’s modeling of how changes in debt influence the economy over time. The “convex” dynamic projection corresponds to the alternative, simpler method described above for incorporating debt effects. In each case, the economy is assumed to be permanently 40 percent open (in both debt and capital).2 As a comparison, the “static” projection is shown that corresponds to conventional forecasts often used in policy analysis that do not allow GDP and capital to change in response to fiscal policy, including a growing debt over time.

Notice that the “in-model” and “convex” approaches are fairly close for the first 10 years. Kinks in early years are due to expiring provisions in the Tax Cuts and Jobs Act, especially related to changes to the tax treatment of investment. However, in the long-run, the differences widen. By 2040, PWBM’s in-model capital is 5.1 percent lower compared to the alternative convex estimate, which pulls GDP down by 1.4 percent relative to the convex approach. The reason is that households in the in-model approach correctly fully incorporate the steep rising debt path, which is only approximated by the convex approach.

As such, PWBM’s modeling approach applies a useful enhancement to common “model blending” methods. PWBM’s approach is especially important with growing debt paths.

-

In more technical terms, the difference follows Jensen’s Inequality. Convexification works well at modest second derivatives but becomes less accurate as the second derivative increases in value. As an example, see the figure here. ↩

-

Consistent with our previous dynamic analysis and the empirical evidence, our baseline assumes that the U.S. economy is 40 percent open and 60 percent closed. Specifically, 40 percent of new government debt is purchased by foreigners. ↩

Year,Static,Convex,In-Model 2017,1.022448941,1.022448941,1.022448941 2018,1.034979173,1.032189042,1.032720238 2019,1.073919301,1.03061762,1.031121098 2020,1.09337552,1.066759105,1.064987923 2021,1.120000807,1.085878385,1.08014423 2022,1.130783306,1.060692242,1.048042232 2023,1.15776592,0.983801929,0.970699598 2024,1.172606009,0.959533144,0.943450602 2025,1.191453665,0.935016476,0.917027987 2026,1.214795342,0.920629791,0.901860143 2027,1.229857816,0.907399649,0.890233193 2028,1.263184743,1.205569269,1.193170987 2029,1.282154246,1.224478472,1.208102441 2030,1.293990261,1.220063473,1.200499515 2031,1.313906491,1.229835711,1.206644163 2032,1.349565917,1.252204425,1.224847799 2033,1.354087894,1.243557477,1.212810356 2034,1.391383441,1.265054217,1.229874437 2035,1.402545444,1.261882805,1.222554194 2036,1.439479676,1.280707995,1.236315361 2037,1.447533076,1.273338647,1.224618731 2038,1.473563438,1.281304442,1.227382149 2039,1.504474302,1.292705784,1.232766489 2040,1.52380527,1.293403821,1.227497001

Year,Static,Convex,In-Model 2017,1.002987998,1.002987998,1.002987998 2018,1.029490661,1.035305914,1.035412054 2019,1.035112682,1.034990668,1.035388953 2020,1.045406082,1.048614361,1.048885042 2021,1.040625534,1.045601606,1.045902414 2022,1.050471452,1.057794626,1.057806405 2023,1.048972279,1.045871471,1.046029951 2024,1.050842082,1.044897533,1.045264249 2025,1.056359689,1.046035035,1.047153413 2026,1.054416056,1.039585221,1.041669511 2027,1.067756883,1.046380615,1.050854619 2028,1.06854837,1.072649497,1.073781382 2029,1.063244933,1.068229822,1.069175385 2030,1.064425268,1.067939275,1.069002391 2031,1.07793661,1.081064365,1.08216952 2032,1.066336755,1.068998919,1.070173966 2033,1.080295973,1.082340801,1.08366049 2034,1.073646398,1.075121091,1.076545339 2035,1.086421296,1.087350784,1.088904448 2036,1.077133745,1.077410891,1.079098669 2037,1.081081352,1.080728548,1.082577861 2038,1.088235066,1.087230385,1.089285138 2039,1.086715386,1.08509622,1.087309141 2040,1.089615661,1.087353581,1.089798903

Year,Static,Convex,In-Model 2017,19390.605,19390.605,19390.605 2018,20247.15208,20303.8146,20308.84245 2019,21071.91739,20774.781,20786.22065 2020,21886.70587,21746.74496,21739.43804 2021,22566.13098,22398.22193,22364.36253 2022,23363.6766,22956.859,22872.59604 2023,24134.76401,22740.14256,22689.02431 2024,24890.28836,23084.07122,23035.47653 2025,25756.13379,23446.25659,23426.93652 2026,26560.59686,23784.83623,23810.46997 2027,27582.29301,24344.54612,24453.29864 2028,28564.21803,28180.00494,28106.25113 2029,29350.40459,28978.24248,28868.48128 2030,30218.84506,29675.95675,29541.6182 2031,31414.10957,30762.96579,30596.59579 2032,32287.66955,31512.90053,31314.7026 2033,33435.30346,32501.97654,32272.02878 2034,34474.38032,33381.60107,33116.93518 2035,35729.52787,34455.93453,34150.81049 2036,36766.84981,35300.51745,34955.28918 2037,37870.67512,36197.91165,35810.14488 2038,39248.3688,37342.72218,36906.75436 2039,40505.02051,38356.90588,37866.40282 2040,41797.63644,39388.22328,38839.24656