Key Points

- Tax benefits for higher education make up 17 percent of federal aid for postsecondary students.

- Families find it difficult to take advantage of tax benefits for higher education. About 14 percent of families do not take benefits for which they qualify. Evidence that tax benefits for higher education induce more students to go to school is weak.

- The authors explore the potential impact of different simplification strategies, providing a roadmap for future empirical work.

Tax Benefits for College Attendance

Editor’s Note: This article is part of a series of tax-related articles sponsored by the Penn Wharton Budget Model and the Robert D. Burch Center at Berkeley. All of the articles in this series are forthcoming in a book by Oxford University Press, co-edited by Alan Auerbach and Kent Smetters.

Tax Benefits for College Attendance examines current tax benefits for higher education, who receives these benefits, if these benefits are effective at expanding college enrollment and potential reforms. Susan Dynarski and Judith Scott-Clayton (2016) find that tax benefits for higher education are complex and difficult for families to navigate and that there is only limited evidence that these expenditures result in more college enrollments.

Federal Support for Postsecondary Students

The U.S. federal government has many programs that support higher education. Programs include land grants to states to fund public universities, loans and grants for students, and tax breaks for universities, students and their families, and school donors.

Optimal Investment in Education

Without financial aid, students might underinvest in education for several reasons. First, education provides benefits to society as well as individuals. A highly educated public may benefit society by increasing civic participation. These social factors--what economists call “externalities”--are generally not incorporated into one’s own decision-making, resulting in too little individual of their investment.

Second, “liquidity constrained” students may not be able to borrow enough against future income to afford the cost of school. To be sure, private markets could provide loans. Nobel Prize laureate Milton Friedman once even suggested that firms purchase “equity” in a student’s future income, as a way of paying for college. But private markets face various challenges in providing and enforcing these loans or equity agreements without some government support.

Third, potential students may underestimate the value of education because the benefit of higher earnings is received years after the decision to enroll. Economists refer to this problem as “present bias,” where people place a larger weight on current consumption relative to future consumption, even against what they know is best for them. A large literature has documented the importance of present bias in influencing personal finance decisions.

Fourth, financial aid also addresses a “gaming problem,” coined the “Samaritan’s Dilemma” problem by Nobel Prize laureate, James Buchanan. In particular, the government can’t credibly precommit to not helping redistribute money to people who choose not to increase their skills. In other words, spending money to teach someone to fish might be more effective than simply giving them fish on an ongoing basis.

Tax Benefits for Higher Education

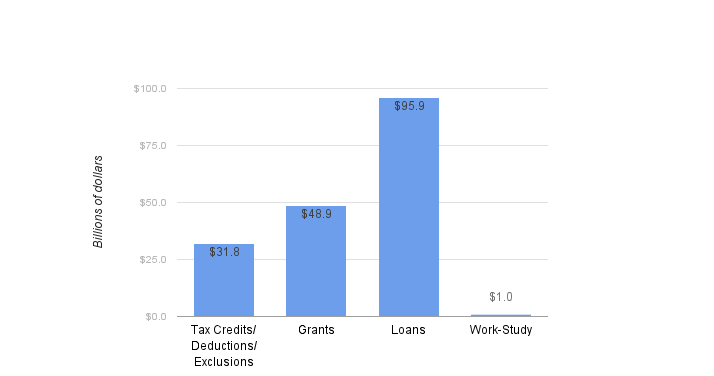

Tax benefits for higher education compose a large portion of federal support for college. As shown in Figure 1, in 2013, at $31.8 billion tax benefits accounted for 17 percent of federal support to students, which totaled $182.9 billion. Tax benefits are similar in size to the Pell Grant program, which, in 2013, was $33.7 billion.

Figure 1: Federal Support for Postsecondary Students by Source, 2031

Source: College Board (2014) for grants, loans and work study, and Crandall-Hollick (2014a) for tax benefits. All values in 2013 constant dollars.

Tax Benefits for Higher Education are Complex

There are more than a dozen tax breaks for education. Figure 2 shows the estimated value of 10 tax expenditures aimed exclusively at higher education. In 2015, credits for tuition made up more than six of every 10 dollars of tax expenditures for higher education.

Figure 2: Estimated Tax Expenditures on Tax Benefits Exclusively for Higher Education (in Billions), 2015

Source: Joint Committee on Taxation (2015a). To adjust reported amounts for recent changes as a result of the Protecting Americans from Tax Hikes (PATH) Act of 2015, budget impact estimates from the Joint Committee on Taxation (2015b) are also incorporated. See Crandall-Hollick (2016) for additional notes on the higher education tax benefits.

Students and their families must navigate a complex web of numerous programs to determine benefits for which they qualify. Several related problems emerge from this complexity.

First, many families appear to not know about various tax benefits for education. The Government Accountability Office (GAO) found that 14 percent of families did not claim benefits for which they qualify.

Second, taking one type of benefit may disqualify a student from taking another. As a result, students and families must determine the optimal combination of benefits to take. For instance, families cannot take both the tuition tax deduction and one of the education tax credits. In fact, the GAO also found that 15 percent of families could have chosen a better combination of benefits.

Third, students and families must also factor in how taking different benefits, or using different forms of payment, will impact their eligibility for financial aid. For example, most families do not have enough money in their 529 education savings accounts to fully pay for college. Spending the 529 money during the junior or senior year of college tends to reduce financial aid less than spending that money during the freshman year. Moreover, 529 plans held by grandparents of the student, rather than the student’s parents, have no impact on financial aid.

Who Benefits from Tax Expenditures for Higher Education?

Some tax expenditures are used across the income distribution while others are concentrated at certain incomes. Use of the American Opportunity Tax Credit (AOTC) is broadly spread across the income distribution. In 2012, families with incomes above $100,000 and families with incomes below $25,000 each received about 24 percent of expenditures for education tax credits and deductions. Families who file jointly with income above $180,000 are not eligible. The AOTC reaches families with low tax liabilities because it is partially refundable. In addition, the AOTC helps students who have their tuition covered by Pell Grants because it includes expenses on books, supplies and equipment.

Savings incentives such as Coverdell accounts and 529 plans are used more by higher-income families than lower-income families. Low-income families may find that saving in advance for college is risky if it is not certain their child will attend college. Higher-income families may be less worried about the impact of assets held in education savings accounts on financial aid eligibility. Finally, the incentive to shield income from taxes is stronger for families in higher marginal tax brackets.

Do Tax Benefits Increase College Enrollment?

The more than $30 billion in tax expenditures for higher education may be an efficient public investment if more people go to school. However, evidence that tax expenditures increase college enrollment is weak. One study finds that more adults whose education fell below their expectations as a teenager went to school after tax credits were introduced in 1998 than before. Another study shows that every additional $100 in tax expenditures for education increased college enrollments by 0.4 percentage points, similar to findings for grant aid. Nonetheless, recent research using large administrative data finds no impact on enrollment. Two recent studies, using detailed IRS data, find that the AOTC and tuition deduction do not increase enrollment, tuition paid or student loans taken.

The Open Question: Would Simplification Increase Education Attainment?

Naturally, some of the difficulty with current programs may be addressed by policy reforms aimed at reducing complexity, aligning the timing of school costs with the receipt of benefits and reducing the administrative burden. Susan Dynarski and Judith Scott-Clayton explore the potential impact of different simplification strategies, providing a roadmap for future empirical work.

For example, if the various tax credits, deductions and exemptions were consolidated, students might find them easier to value. If the tax benefits were easy to value it could make the cost of school more certain and understandable and perhaps increase enrollment and program effectiveness. One way to simplify benefits is to reduce the current long list of tax benefits for higher education to a single refundable tax credit.

Integrating tax credits for higher education with the Pell Grant program could also reduce administrative burdens for government, schools, and students and families while aligning the timing of costs and benefits. Families could fill out only one form. The Internal Revenue Service (IRS) could send the information needed to determine eligibility to the Department of Education who could use their existing systems to deliver funds to schools. In addition, the combined program might increase the impact of tax benefit programs on enrollment because students and families would receive tax education benefits at the same time as school tuition bills.

Conclusion

Federal benefits for students cost more than $180 billion a year and are complex, difficult to administer. Evidence shows that these program are not utilized optimally. Future empirical work is needed to explore the potential value of reducing complexity and simplifying the financial aid process.

A discussion of this paper is provided by David Figlio.