Effective Tariff Rates and Revenues (Updated June 16, 2026)

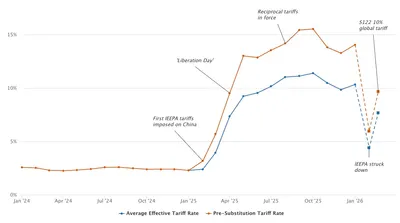

The USITC recently released updated trade and tariff data. As of April 2026, the effective tariff rate stood at 7.0 percent.

7 items found

The USITC recently released updated trade and tariff data. As of April 2026, the effective tariff rate stood at 7.0 percent.

The USITC recently released updated trade and tariff data. We estimate an effective tariff rate of 7.1 percent as of March 2026, the first full month after the IEEPA tariffs were replaced by a global 10 percent tariff implemented under Section 122.

The USITC recently released updated trade and tariff data. We estimate an effective tariff rate (ETR) of 10.3 percent through January 2026. We project that replacing the IEEPA tariffs with a new 10% global tariff rate lowers the ETR to 7.7 percent on a bias-corrected basis appropriate for short-term projections.

We project that reversing the IEEPA tariffs will generate up to $175 billion in refunds. Unless replaced by another source, future tariff revenue collections will fall by half.

We project that corporate tax revenue will decrease by $276 billion over 10 years on a conventional basis due to changes in international tax provisions related to the Section 250 deduction under OBBBA.

The OECD expects countries to implement components of Pillar Two, its framework for a global minimum tax, starting in 2024. This paper provides policymakers with a comprehensive resource for navigating the Pillar Two framework. We review key components of Pillar Two and related aspects of US tax policy, including: (i) how the global minimum tax is likely to expose portions of the current US corporate tax base to new foreign taxes; (ii) potential modifications to US tax law that would increase compliance and protect US tax rights; and, (iii) the extent to which Pillar Two is likely to succeed in its policy objectives of reducing corporate profit shifting and international tax competition. The US is likely to cede tax rights to foreign jurisdictions if it does not enact new tax law. Pillar Two will likely reshape the nature of tax competition between countries, incentivizing greater use of subsidies and refundable tax credits to counteract higher statutory rates.

We estimate that each month of school closures in response to the COVID pandemic cost current students between $12,000 and $15,000 in future earnings due to lower educational quality. We also estimate total value-of-life, medical, and productivity costs per infection at $38,315 for September 2020. Using these costs, we calculate the cost-benefit threshold to keeping schools closed for October at over 0.355 new expected infections in the community per student kept out of school.