Effective Tariff Rates and Revenues (Updated July 13, 2026)

The USITC recently released updated trade and tariff data. As of May 2026, the effective tariff rate stood at 7.2 percent.

12 items found

The USITC recently released updated trade and tariff data. As of May 2026, the effective tariff rate stood at 7.2 percent.

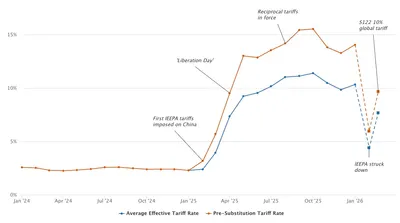

The USITC recently released updated trade and tariff data. We estimate an effective tariff rate of 7.1 percent as of March 2026, the first full month after the IEEPA tariffs were replaced by a global 10 percent tariff implemented under Section 122.

The USITC recently released updated trade and tariff data. We estimate an effective tariff rate (ETR) of 10.3 percent through January 2026. We project that replacing the IEEPA tariffs with a new 10% global tariff rate lowers the ETR to 7.7 percent on a bias-corrected basis appropriate for short-term projections.

We project that reversing the IEEPA tariffs will generate up to $175 billion in refunds. Unless replaced by another source, future tariff revenue collections will fall by half.

We estimate that importers avoided 13.1 percent ($6.5 billion) of new tariffs by accelerating purchases and changing their purchasing patterns in response to the new tariff regime. Importers especially stockpiled pharmaceuticals and precious metals during 2025 Q1.

We examine recent capital market dynamics in the context of budget reconciliation and trade policies. Understanding these dynamics requires modeling the interaction between microeconomic behavior and macroeconomic outcomes—an approach particularly well suited for the overlapping-generations lifecycle model.

Treasury data through April 28 shows that tax receipts are broadly in line with government projections made earlier this year, before the downsizing of the IRS was announced. Receipts from tariffs have significantly exceeded projections.

Many trade models fail to capture the full harm of tariffs. PWBM projects Trump’s tariffs (April 8, 2025) will reduce long-run GDP by about 6% and wages by 5%. A middle-income household faces a $22K lifetime loss. These losses are twice as large as a revenue-equivalent corporate tax increase from 21% to 36%, an otherwise highly distorting tax.

Using more recent data on international capital flows, we find that the “effective openness” of the U.S. economy has decreased to 31.5 percent openness for private capital flows and 33.3 percent U.S. debt take-up by foreigners. This decline is in line with our prediction from last year’s posts on the effect of tariffs.

PWBM’s Efraim Berkovich, the Wharton School’s Marshall Meyer and Mary Lovely of the Maxwell School of Syracuse University discussed how the recently imposed tariffs on Chinese goods are raising prices for consumers, disrupting supply chains and weighing down economic growth in the long-run.

We find that, excluding times of intervention by the Federal Reserve, interest rates on U.S. government debt are higher when levels of effective openness to foreign capital flows are lower, increasing the government’s borrowing costs.

We project that even if the recently imposed tariffs are removed, GDP will be permanently smaller relative to having had no trade war. Extending the current trade war by several more years will lead to smaller losses in GDP in 2020 but will reduce GDP by more in the long run.