Effective Tariff Rates and Revenues (Updated June 16, 2026)

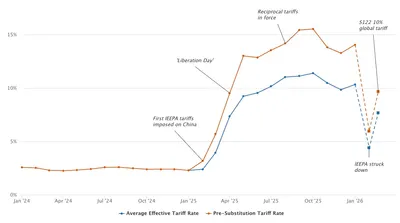

The USITC recently released updated trade and tariff data. As of April 2026, the effective tariff rate stood at 7.0 percent.

124 items found

The USITC recently released updated trade and tariff data. As of April 2026, the effective tariff rate stood at 7.0 percent.

The USITC recently released updated trade and tariff data. We estimate an effective tariff rate of 7.1 percent as of March 2026, the first full month after the IEEPA tariffs were replaced by a global 10 percent tariff implemented under Section 122.

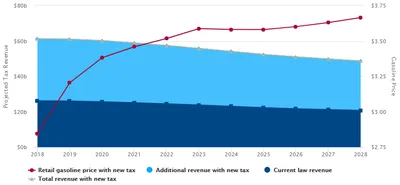

A four-month federal gas tax suspension would cost the Highway Trust Fund roughly $11.5 billion in lost revenue, with consumers seeing only partial price relief.

Projected per-gallon price drops and two-month revenue losses if states suspend gasoline and diesel taxes.

We project that Social Security's Old-Age and Survivors Insurance Trust Fund will deplete in six years (2032). We consider five different reform options that vary in the amount of tax increases and benefit cuts. Traditional policy analysis that dominates federal policymaking often provides very different — even opposite — insights compared to more comprehensive modeling.

The USITC recently released updated trade and tariff data. We estimate an effective tariff rate (ETR) of 10.3 percent through January 2026. We project that replacing the IEEPA tariffs with a new 10% global tariff rate lowers the ETR to 7.7 percent on a bias-corrected basis appropriate for short-term projections.

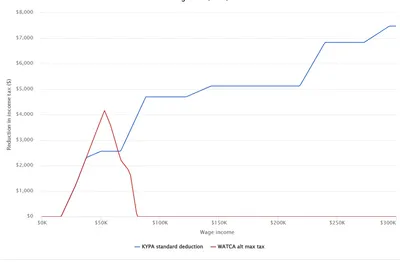

Two Senate proposals widen the zero tax bracket — Senator Booker's KYPA through a doubled standard deduction (costing $5.1 trillion) and Senator Van Hollen's WATCA through an alternative maximum tax (costing $1.4 trillion) — illustrating how mechanism determines cost, targeting, and distortions.

Senator Van Hollen's Working Americans' Tax Cut Act would pair a new alternative maximum tax for low- and middle-income filers with a graduated millionaire surtax, increasing federal revenue by $264 billion over a decade, not including economic feedback effects.

We estimate that the Keep Your Pay Act proposed by Senator Cory Booker would reduce federal revenues by up to $6.4 trillion over a decade. Households earning $100,000–$200,000 receive the largest tax cuts. Separately, on social media, Senator Booker proposed a top-rate increase that we estimate would offset about $1.4 trillion.

We project that reversing the IEEPA tariffs will generate up to $175 billion in refunds. Unless replaced by another source, future tariff revenue collections will fall by half.

Revenue and distributional effects of lowering the cap on the marginal tax benefit of itemized deductions to 32% or 24%.

We project that corporate tax revenue will decrease by $276 billion over 10 years on a conventional basis due to changes in international tax provisions related to the Section 250 deduction under OBBBA.

PWBM estimates that the COVID-era Employee Retention Credit (ERC) will have cost more than $300 billion when the IRS finishes processing claims later in 2025, nearly four times the initial projected cost. Most of the ERC was paid retroactively, well after pandemic-related economic disruptions had ended, limiting its effectiveness as a worker retention incentive.

It is well known that mass deportation reduces aggregate economic variables like GDP due to scale effects. We project that deportation also reduces wages of high-skill workers, compromising 63% of workers. Still, authorized low-skilled workers can see their wages increase but only if the deportation policy is permanently sustained after 4 years. Even with new funds provided in the 2025 OBBBA, we estimate that permanent deportation would cost an additional $900 billion over the first 10 years.

We estimate that importers avoided 13.1 percent ($6.5 billion) of new tariffs by accelerating purchases and changing their purchasing patterns in response to the new tariff regime. Importers especially stockpiled pharmaceuticals and precious metals during 2025 Q1.

We estimate the reconciliation bill signed by President Trump increases primary deficits by $3.2 trillion over 10 years. The dynamic cost, including changes to the economy, is larger at $3.6 trillion. GDP falls by 0.3 percent in 10 years and 4.6 percent in 30 years.

For the final bill, please see our analysis of the President Trump-Signed Reconciliation Bill .

For the final bill, please see our analysis of the President Trump-Signed Reconciliation Bill .

We examine recent capital market dynamics in the context of budget reconciliation and trade policies. Understanding these dynamics requires modeling the interaction between microeconomic behavior and macroeconomic outcomes—an approach particularly well suited for the overlapping-generations lifecycle model.

For the final bill, please see our analysis of the President Trump-Signed Reconciliation Bill .

If spending and tax changes in Reconciliation are made permanent, federal debt increases by 11.1 percent in 10 years and 24.3 percent in 30 years. GDP remains flat and wages fall by 0.5 percent. Dynamic costs exceed conventional costs in the budget window.

We estimate the House reconciliation bill increases primary deficits by $3.3 trillion over 10 years. Even so, GDP rises in the short and long term, as precautionary increases in labor supply and savings respond to a reduced social safety net.

For the final bill, please see our analysis of the President Trump-Signed Reconciliation Bill .

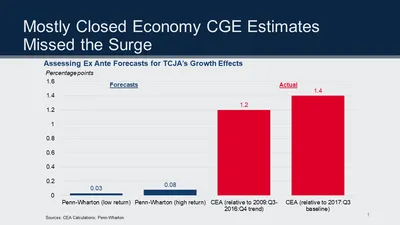

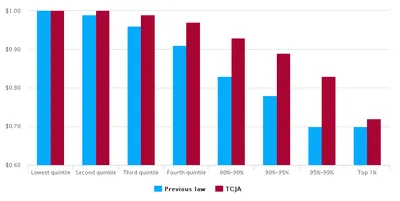

Under current law, the 2017 Tax Cuts and Jobs Act (TCJA) will expire at the end of 2025, raising personal income tax rates back to 2017 levels. Some lawmakers propose extending the TCJA but with higher rates for high-income households. We consider three options.

Treasury data through April 28 shows that tax receipts are broadly in line with government projections made earlier this year, before the downsizing of the IRS was announced. Receipts from tariffs have significantly exceeded projections.

Many trade models fail to capture the full harm of tariffs. PWBM projects Trump’s tariffs (April 8, 2025) will reduce long-run GDP by about 6% and wages by 5%. A middle-income household faces a $22K lifetime loss. These losses are twice as large as a revenue-equivalent corporate tax increase from 21% to 36%, an otherwise highly distorting tax.

For the final bill, please see our analysis of the President Trump-Signed Reconciliation Bill .

Eliminating taxes on Social Security benefits reduces incentives to save and work while increasing federal debt. Wages and GDP fall over time. The policy primarily benefits high-income households nearing or in retirement while harming households under thirty and all future generations across the entire income distribution.

Treasury debt held by the public is an explicit pay-as-you-go obligation. The government also runs implicit pay-as-you-go obligations, such as Social Security and Medicare Part A, which are twice as large. Both types of obligations require tax increases and spending cuts to balance the budget over time.

The deduction for pass-through income under section 199A provides a benefit in excess of 20 percent (“excess benefit”) for some taxpayers due to its interaction with the progressive tax rate system. As Congress considers extending 199A beyond 2025, options to remove the excess benefit while maintaining the 20 percent tax benefit could raise between $46B and $178B over the 10-year budget window, depending on design.

A package of 13 major tax and spending reforms, based on standard public economics design principles, is shown to reduce federal debt, increase social insurance, and expand the economy more than any previously analyzed policies by PWBM.

We analyze new data from the US Treasury to examine historical revenue effects of TCJA’s international corporate tax provisions. We also provide updated conventional estimates to assess the revenue impact of scheduled 2026 rate increases on foreign income of US corporations and assess several proposals that aim to further increase tax revenue.

We explain how the PWBM uses its dynamic Overlapping Generation (OLG) model to analyze tax policies affecting foreign-earned income by affiliates of U.S.-domiciled firms. We evaluate two illustrative policy changes: we show how firms’ tax liabilities and the allocation of capital between domestic and international production are affected by an increase in foreign tax rates and a decrease in U.S. tax exemptions on foreign-derived income.

We examine two major investment tax incentives for the computer sector. The impact on computer-sector investment as well as economy-wide investment is very small, even when the computer sector is modeled as a production complement.

After Ireland ended the Double Irish tax planning strategy in 2020, US firms with historical links to Ireland have shifted their intellectual property (IP) away from traditional tax havens to Ireland and the US to take advantage of tax incentives offered by both countries. This has coincided with a significant increase in Irish corporate tax revenue, particularly for less capital-intensive firms. Repatriation of foreign earnings to the United States has also increased, but fiscal benefits to the US have been offset by tax incentives passed under TCJA.

The impact of income-driven repayment (IDR) educational financing plans by income, race, and gender is not generally well understood. Our analysis estimates that approximately 43 percent of the subsidies from President Biden’s Saving on a Valuable Education (SAVE) plan will accrue to current Black student borrowers and 71 percent to current female borrowers. While lower- to middle-income student borrowers stand to gain the most, we estimate that about a fifth of the benefits will go to households in the top 20 percent of the income distribution, and borrowers with graduate-level education who benefit from the SAVE plan tend to experience the highest savings on average.

Note: This document was updated on 5/30/2024 to include a discussion of how much of the policy would be paid for by economic feedback effects.

We examine recent trends in the activities of US multinationals and their foreign affiliates using data from the Bureau of Economic Analysis’s annual survey of US direct investment abroad. Since the passage of the Tax Cuts and Jobs Act (TCJA), multinational activity has become more domestically concentrated, continuing a trend that started before the legislation. This has coincided with a decline in the US effective corporate tax rate and relatively stable foreign effective tax rates.

PWBM estimates that the Wyden-Smith tax proposal ( H.R. 7024 ) would reduce revenues by $3 billion over the next decade on a conventional basis.

We report estimates from the Penn Wharton Budget Model (PWBM) that exempting employment-based green cards from statutory limits for applicants (and their families) who have earned a doctoral or master’s degree in a STEM field---similar to Section 80303 in H.R. 4521---would reduce federal budget deficits by $129 billion from 2025 to 2034. In contrast, a conventional budget estimate, which would include projected increases in federal spending but not the effect of a larger population on federal tax revenues, shows an increase in federal deficits of $4 billion.

The House of Representatives is considering legislation that would rescind $14.3 billion of IRS funding as a budgetary offset for a package that provides aid to Israel. CBO estimates that the decrease in IRS funding alone would reduce revenue by $26.8 billion over 10 years, increasing the deficit by $12.5 billion. Due to scoring conventions, CBO’s projected deficit increase could not be reversed for any future legislation that adds the $14.3 billion in funding back to the IRS.

The OECD expects countries to implement components of Pillar Two, its framework for a global minimum tax, starting in 2024. The US is likely to cede tax rights to foreign jurisdictions if it does not enact new tax law. Pillar Two will likely reshape the nature of tax competition between countries, incentivizing greater use of subsidies and refundable tax credits to counteract higher statutory rates.

The OECD expects countries to implement components of Pillar Two, its framework for a global minimum tax, starting in 2024. This paper provides policymakers with a comprehensive resource for navigating the Pillar Two framework. We review key components of Pillar Two and related aspects of US tax policy, including: (i) how the global minimum tax is likely to expose portions of the current US corporate tax base to new foreign taxes; (ii) potential modifications to US tax law that would increase compliance and protect US tax rights; and, (iii) the extent to which Pillar Two is likely to succeed in its policy objectives of reducing corporate profit shifting and international tax competition. The US is likely to cede tax rights to foreign jurisdictions if it does not enact new tax law. Pillar Two will likely reshape the nature of tax competition between countries, incentivizing greater use of subsidies and refundable tax credits to counteract higher statutory rates.

Despite a complete overhaul of the US system of international corporate taxation in the Tax Cuts and Jobs Act of 2017, taxes on US corporations’ foreign income are about the same after the law’s enactment as before.

PWBM estimates that Title I of the Build It in America Act would add $76 billion to the budget deficit over the next decade and reduce deficits by $18 billion during the subsequent second decade. It would temporarily boost business investment and GDP during the next two years while lowering GDP in subsequent years. If lawmakers made the extensions permanent, the budgetary cost would rise to $1.25 trillion over the next two decades and GDP would largely remain unchanged, as the tax incentive effects and debt effects mostly offset.

PWBM estimates the Tax Cuts for Working Families Act would reduce federal revenues by $96 billion over a decade, cutting taxes for a majority of households in 2024. Households in the bottom quintile households, and those in the top 1 percent, generally would not benefit. As an illustration, we also consider making the provisions permanent, which raises the estimated ten-year budget cost to be between $419 billion and $527 billion.

The deadline to raise the nation’s debt ceiling is closer than previously thought because tax receipts in April fell below projections. PWBM estimates that receipts are running $150 billion below government projections for fiscal year 2023, most likely due to a decline in capital gains income and weakening corporate profit margins.

Several revenue and spending provisions in The Tax Cuts and Jobs Act (TCJA) are scheduled to expire (“sunset”) by the end of 2025. We estimate that “extenders” (“no sunset”) would increase the federal debt held by the public from 226.0 percent of GDP to 261.1 percent of GDP by 2050.

President Biden has proposed raising the current excise tax rate on stock repurchases from 1 percent to 4 percent. We estimate that, for domestic shareholders, this tax increase would eliminate about 85 percent of the current-law tax preference for dividends over stock repurchases.

We estimate that forgiving federal college student loan debt will cost between $300 billion and $980 billion over the 10-year budget window, depending on program details. About 70 percent of debt relief accrues to borrowers in the top 60 percent of the income distribution.

PWBM estimates that the Senate-passed version of the Inflation Reduction Act would reduce non-interest cumulative deficits by $264 billion over the budget window. The impact on inflation is statistically indistinguishable from zero. GDP falls slightly within the first decade while increasing slightly by 2050. Most, but not all, of the tax increases fall on higher income households.

PWBM and CBO find an almost identical impact of the Inflation Reduction Act of 2022 (“IRA”) on the budget, with small differences stemming from the timing of the corporate minimum tax revenue. The impact on inflation is statistically indistinguishable from zero for either estimate.

PWBM estimates that the Inflation Reduction Act would reduce non-interest cumulative deficits by $248 billion over the budget window with no impact on GDP in 2031. The impact on inflation is statistically indistinguishable from zero. An illustrative scenario is also presented where Affordable Care Act subsidies are made permanent. Under this illustrative alternative, the 10-year deficit reduction estimate falls to $89 billion.

We estimate that the federal estate tax would have generated 9 times more revenue in 2019 without the tax changes in 2001 and 2017.

We estimate that suspending the federal excise tax on gasoline from July to September this year would lower average gasoline spending per capita by between $4.79 and $14.31 over three months, depending on geographic location and modeling assumptions, and lower federal tax revenue by about $6 billion during that period.

We estimate that the U.S. federal government faces a permanent fiscal imbalance equal to over 10 percent of all future GDP under current law where future federal spending outpaces tax and related receipts. Federal government debt will climb to 236 percent of GDP by 2050 and to over 800 percent of GDP by year 2095 (within 75 years).

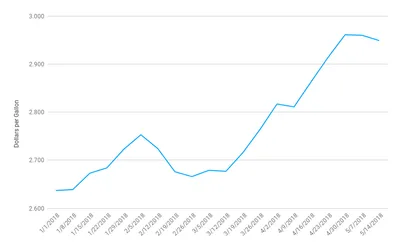

We provide causal evidence that recent suspensions of state gasoline taxes in three states were mostly passed onto consumers at some point during the tax holiday in the form of lower gas prices: Maryland (72 percent of tax savings passed onto consumers), Georgia (58 percent to 65 percent) and Connecticut (71 percent to 87 percent). However, these price reductions were often not sustained during the entire holiday.

Households owed more than $500 billion in taxes when they filed their returns this year, an increase of about $200 billion from immediately prior to the pandemic. The large tax liability owed at filing is mostly the result of a surge in capital gains and other income from financial assets in 2021.

We estimate that suspending the federal gas tax from March to December 2022 would lower average gasoline spending per capita between $16 and $47, depending on geographic location and assumptions, but lower federal tax revenue by about $20 billion over that period.

This brief examines different approaches to removing the capital gains “lock-in effect” within a realization-based tax framework. We estimate that this change would produce between $115 billion and $357 billion in additional tax revenue over the next 10 years, depending on the exact design.

PWBM projects that the spending and taxes in the Build Back Better Act (H.R. 5376), as written, would add up to 0.2 percentage points to inflation over the next two years and reduce inflation by similar amounts later in the decade. As an illustrative alternative, if temporary major spending provisions were made permanent, the bill would add up to a third of a percentage point to near-term inflation and have a negligible impact on inflation later in the decade.

PWBM projects that Sen. Wyden’s billionaire income tax proposal would raise $507 billion over the budget window, more than half of which would come from a one-time transition tax on previously accrued, unrealized capital gains on publicly traded assets.

PWBM estimates that the White House’s Build Back Better reconciliation framework would increase spending by $1.87 trillion over the 10-year budget window and revenues by $1.56 trillion over the same period. By 2050, the proposal would increase federal debt by 2.0 percent and decrease GDP by 0.1 percent, relative to the current law baseline.

PWBM projects the House Ways and Means Committee proposal to temporarily extend the 2021 Child Tax Credit design would provide an average 2022 refundable tax cut of $2,785 to 78 percent of households with children at a budgetary cost of $545 billion over the 10-year budget window. Changes to phase-out and phase-in thresholds would reduce the budgetary cost but also reduce the size of the tax cuts.

Higher inflation reduces the real value of the government’s outstanding debt while increasing the tax burden on capital investment due to lack of inflation indexing. Increasing the current annual inflation target regime from 2 percent to 3 percent inflation reduces debt while lowering GDP.

PWBM estimates that tax policy changes in low-tax countries in response to the recent OECD global minimum tax deal could cost the U.S. as much as 50 percent of its minimum tax revenue.

PWBM projects that the long-run aggregate macroeconomic effects of Senator Joe Manchin's $1.5T reconciliation framework would be negligible. The economic benefits would largely accrue to younger, poorer households while the economic costs would fall mostly on richer households.

We project that recent tax reforms proposed by the House Ways and Means Committee would increase the incentive of U.S. firms to shift intangible investments and profits to foreign countries with a tax rate below 20.7 percent.

The House Ways and Means Committee reforms proposed as part of budget reconciliation would increase the U.S. statutory corporate income tax rate to 26.5 percent, bringing the combined federal and state rate to 30.9 percent, making the U.S. rate the third highest among OECD members.

The House Ways and Means Committee reforms proposed as part of budget reconciliation would more than triple the U.S. tax rate on multinationals’ foreign income and produce a higher rate than a proposed global agreement currently being negotiated through the OECD.

PWBM projects that the revenue-raising provisions in the House Ways and Means Reconciliation Bill would raise roughly $2.4 trillion from 2022 to 2031.

We analyze a combination of net revenue raisers consistent with the requirements released by the Senate Budget Committee on August 9th, 2021, for budget reconciliation.

The bipartisan Senate infrastructure deal, endorsed by President Biden, authorizes about $548 billion in additional infrastructure investments, which we estimate is funded by $132 billion in new tax provisions and $351 billion in new deficits. We project that proposal would have no significant effect on GDP by end of the budget window (2031) or in the long run (2050).

We estimate that the recent OECD proposal for a global minimum tax would triple the effective U.S. tax rate on foreign income from 2 percentage points to 5.8 percentage points. The Biden administration’s proposed changes to the U.S. global minimum tax regime would instead raise the effective U.S. tax rate on foreign income to 12.4 percentage points.

Households in the top 5 percent of the income distribution receive inheritances between 4 to 12 times larger than households in the bottom 80 percent, depending on the exact definition of inheritance used.

Under current law, PWBM projects that U.S. multinationals will report a cumulative $3.6 trillion in Global Intangible Low-Taxed Income (GILTI) between 2022 and 2031. Data released in July 2021 by the Internal Revenue Service for the 2018 tax year provides the first opportunity for a more extensive validation of PWBM’s model of U.S. multinationals’ tax returns. PWBM projects 2018 GILTI within 5.3 percent of the IRS value, suggesting a very good model fit.

The bipartisan Senate infrastructure deal, endorsed by President Biden, authorizes $1.2 trillion of spending, representing about $579 billion in additional infrastructure investments funded by a mix of deficits, user fees, and other tax provisions. This proposal would increase output in 2050 by 0.1 percent.

PWBM projects that the legalization provisions of the U.S. Citizenship Act proposed by President Biden would increase per capita spending on the Supplemental Nutrition Assistance Program (SNAP) by 1.2 percent in 2031 and 0.7 percent 2050 relative to the current policy baseline. Per capita payroll taxes would increase by 1.3 and 0.2 percent relative to the current policy baseline, in 2031 and 2050 respectively.

PWBM projects that the American Families Plan (AFP) would spend $2.3 trillion, about $500 billion more than the White House’s estimate, over the 10-year budget window, 2022-2031. We estimate that AFP would raise 1.3 trillion in new tax revenue over the same period. By 2050, the AFP would increase government debt by about 4 percent and decrease GDP by 0.3 percent.

PWBM estimates that raising the top statutory rate on capital gains to 39.6 percent would decrease revenue by $33 billion over fiscal years 2022-2031. If stepped-up basis were eliminated—as proposed in President Biden’s campaign plan—then raising the top rate to 39.6 percent would instead raise $113 billion over 2022-2031.

PWBM projects that the American Jobs Plan proposed by President Biden would spend $2.7 trillion and raise $2.1 trillion dollars over the 10-year budget window 2022-2031. The proposal’s business tax provisions continue past the budget window, decreasing government debt by 6.4 percent and decreasing GDP by 0.8 percent in 2050, relative to current law.

PWBM projects that the Ultra-Millionaire Tax Act of 2021, introduced by Senator Elizabeth Warren, would raise $2.1 trillion over the standard 10-year budget window (2022-2031) under scoring conventions used by government agencies. Incorporating the effects of enhanced IRS enforcement, our projection rises to $2.4 trillion over 2022-2031 and $2.7 trillion over 2023-2032. Also incorporating macroeconomic effects of the Act reduces estimated revenue to $2.0 trillion over 2022-2031 and $2.3 trillion over 2023-2032. We estimate that the Act would reduce GDP by 1.2 percent in 2050.

This post compares effective marginal tax rates (EMTRs) under the Family Security Act proposed by Sen. Romney and the Child Tax Credit (CTC) expansion proposed by Rep. Neal and President Biden. Married families with children and less than $45,000 in income would face EMTRs 4.4 percentage points higher under the Romney proposal and 6 percentage points higher under the Biden/Neal proposal.

PWBM estimates that three provisions in the Biden COVID relief plan—direct payments, expanding the Child Tax Credit, and expanding the Earned Income Tax Credit—together would cost $595 billion in calendar year 2021, with 99 percent of households in the bottom 80 percent of incomes receiving a benefit.

The TEACHUP program, proposed by Rick Miller, Ph.D. as part of the PWBM Democratizing the Budget Contest, would give grants to states in order to provide full-day preschool for four-year-old children at or below 200 percent of the poverty line. On a conventional basis, PWBM projects that TEACHUP would cost $92.4 billion over ten years and a total of $282.53 billion by 2050. However, on a dynamic basis that includes productivity effects and expansion of the tax base, PWBM estimates that the program would effectively pay for itself by 2050 by holding public debt nearly constant.

This post is part of a series that explains tax concepts. The highest 1 percent of earners are responsible for 71 percent of capital gains realizations. President Trump has proposed lowering the top rate on income from capital gains and dividends, while former Vice President Joe Biden has proposed increasing the top rate for taxpayers with more than $1 million in income.

PWBM estimates that reducing the top preferential rates on capital gains and dividends from 20 percent to 15 percent will cost $98.6 billion dollars over the ten year budget window. This tax cut will only benefit tax units in the top 5 percent of the income distribution, with 75 percent of the benefit accruing to those in the top 0.1 percent of the income distribution.

PWBM uses dynamic distributional analysis to evaluate the effects of the Biden platform on different age and income groups. We find that working-age individuals in the bottom 40 percent of taxable income benefit the most due to expanded health insurance, increases in housing subsidies, and lower cost of prescriptions in the Biden platform, while young, high-income individuals and wealthy retirees see net losses due to tax increases and lower returns on their savings.

Presidential candidate Joe Biden recently announced a proposal to temporarily expand the Child Tax Credit (CTC). We find that this proposal would cost $110 billion if implemented solely for calendar year 2021 and would cost $1.4 trillion over ten years if extended permanently. While higher income households are more likely to have qualifying children and would see larger average tax cuts ($1160 for the 90-95th percentile), lower income groups would see the largest relative benefit, with after-tax incomes increasing by 9 percent for the bottom quintile.

Using more recent data on international capital flows, we find that the “effective openness” of the U.S. economy has decreased to 31.5 percent openness for private capital flows and 33.3 percent U.S. debt take-up by foreigners. This decline is in line with our prediction from last year’s posts on the effect of tariffs.

We use PWBM’s new dynamic model enhancement of the business sector to analyze several foreign and domestic business taxation provisions from the Biden tax plan. While raising the effective tax rate on foreign profits increases domestic capital, wages, and GDP, provisions that raise domestic business taxes have the opposite effect—when combined, these business tax provisions decrease the capital stock by 0.21 percent and decrease wages by 0.69 percent in 2050.

The CARES Act establishes a new, temporary charitable deduction (limited to $300) in tax year 2020 for taxpayers who claim the standard deduction. PWBM projects that this provision would cost about $2 billion and would have little effect on total donations. More than half (53 percent) of the benefit would accrue to families in the 60th to 90th percentiles of the income distribution.

We present budgetary and distributional estimates for three potential versions of the lump-sum payment that President Trump announced earlier today. All three options increase the after-tax income of low income households the most. However, higher-income households have more children on average and would receive larger cash payments unless additional adjustments are made.

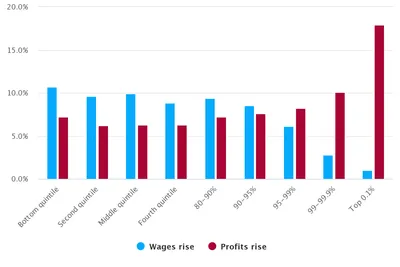

We expand our previous analysis of President Trump’s proposed payroll tax holiday by considering two scenarios for how the employer side of the tax cut would be distributed: either to the full benefit of business owners and corporate equity holders (“profits rise”) or to the full benefit of workers (“wages rise”). When profits rise, the top 1 percent of families by income receive about 29 percent of the total payroll tax cut, compared to about 4 percent of the total cut when wages rise.

Recent revisions to estimates of corporate profits may explain the unanswered question of why corporate income tax receipts have underperformed CBO estimates in recent years.

We estimate the budgetary, economic and distributional effects of raising the Social Security taxable maximum to $300,000 starting on January 1st, 2021. We project that it would raise $1.2 trillion of additional revenue on a conventional basis over the 10-year budget window and lower GDP 1.7 percent by 2050. Families in the top 10 percent of the income distribution would bear 93 percent of the overall burden of this tax increase.

We estimate the budgetary, economic and distributional effects of eliminating all Schedule-A itemized deductions starting on January 1st, 2021. We project that it would raise about $2.1 trillion of additional revenue on a conventional basis over the 10-year budget window and increase GDP by 2.3 percent by 2050. Families in the top 10 percent of the income distribution would bear 75 percent of the overall burden of this tax increase.

Under current law, PWBM estimates that a 33% capital gains tax rate maximizes revenue, but this rate increases to 42% if stepped-up cost basis at death were eliminated.

We estimate the budgetary and economic effects of increasing the top rate on long-term capital gains and qualified dividends from 20 percent to 24.2 percent, which is enacted on January 1st, 2021. We project that it will raise around $60 billion of additional revenue on a conventional basis over the 10-year budget window and increase GDP by 0.1 percent by 2050.

We estimate the budgetary and economic effects of a new broad-based 1 percent value-added tax (VAT) with a progressive universal rebate calculated based on earnings, which is enacted on January 1st, 2021. We project that it will raise $700 billion of additional revenue on a conventional basis over the 10-year budget window and increase GDP by 0.8 percent by 2050.

We estimate the budgetary and economic effects of a new carbon tax of $30 per ton of emissions, which is enacted on January 1st, 2021, rising by inflation plus 5 percent through 2050. We project that it raises $1.6 trillion of additional revenue on a conventional basis over the 10-year budget window and increases GDP by 2.2 percent by 2050.

We estimate that a one-year “payroll tax holiday” would cost the federal government between $141 and $151 billion over the standard budget window and increase GDP by 0.3 percent in 2020, with effects eventually turning slightly negative over time with higher deficits.

PWBM’s Efraim Berkovich, the Wharton School’s Marshall Meyer and Mary Lovely of the Maxwell School of Syracuse University discussed how the recently imposed tariffs on Chinese goods are raising prices for consumers, disrupting supply chains and weighing down economic growth in the long-run.

We find that, excluding times of intervention by the Federal Reserve, interest rates on U.S. government debt are higher when levels of effective openness to foreign capital flows are lower, increasing the government’s borrowing costs.

We project that even if the recently imposed tariffs are removed, GDP will be permanently smaller relative to having had no trade war. Extending the current trade war by several more years will lead to smaller losses in GDP in 2020 but will reduce GDP by more in the long run.

On June 7, Hill staffers, fiscal experts, and PWBM gathered to discuss the federal revenue loss created by tax avoidance. The U.S. has different tax rates for different income streams, thus there are opportunities for individuals and businesses to reduce their tax bills by recharacterizing income to pay a lower rate.

We project that increasing annual net legal immigration leads to a younger and more educated U.S. population. These population changes are likely to have a positive impact on entitlement finances and tax burdens relative to current policy. In contrast, decreasing annual net legal immigration likely has the opposite effects.

By substantially expanding the standard deduction, the Tax Cuts and Jobs Act reduced the incentive to make charitable contributions. We make use of data on non-tax itemizers to examine several potential policies designed to increase tax incentives for charitable giving. In particular, we project that a non-refundable credit for charitable contributions for filers who don’t itemize would expand giving by $208 billion (5.2 percent) and reduce tax revenue by $267 billion (0.6 percent) over the 10 year budget window. Other reforms produce smaller increases in giving along with smaller losses in revenue.

Discussions of genuine tax reform often focus upon broadening the individual and corporate tax bases and lowering tax rates. These discussions also tend to assume that reform will be "revenue neutral", meaning that the new tax structure would generate the same receipts for the government as the old structure. Because firms can currently either incorporate or operate as a pass-through entity, one question that results from these discussions is how firms will react to the relative change in the corporate and non-corporate tax rates. Our results suggest that a 10 percent reduction in the tax wedge between the net corporate and individual tax rate will result in a 0.5 to 0.9 percent increase in the share of positive business income accruing to corporations.

The PWBM Simulator implements micro-level projections of individuals and families in the United States to observed trends and interactions among many demographic and economic variables. Historical estimates and projections are rigorously validated using many sources of micro-data information in the United States. Using PWBM-Simulator output to implement tax policy analysis requires mapping its distributions of individuals and families into distributions of tax filing units with appropriate income elements calibrated to observed features of U.S. tax filers. This paper described the procedures used for augmenting PWBM Simulator's micro projections with tax variables from the IRS's public use tax-return samples –the Statistics of Income surveys.