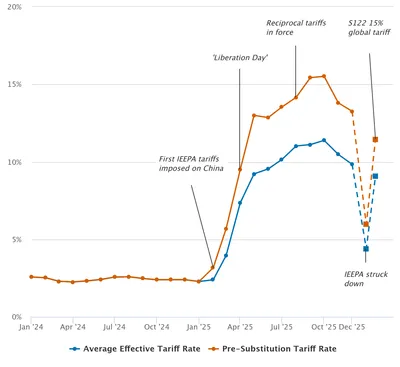

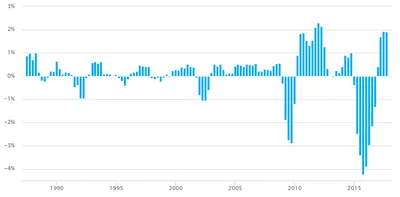

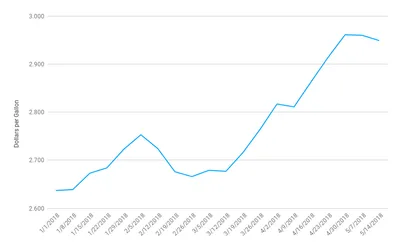

Effective Tariff Rates and Revenues (Updated February 23, 2026)

The USITC recently released updated trade and tariff data . We estimate an effective tariff rate (ETR) of 9.8 percent through December 2025. We project that replacing the IEEPA with a new 15% global tariff rate has only a small impact on the ETR, lowering it to 9.1 percent, on a consistent concept basis.